Sequential decisions in volatile, high-stakes settings require more than

maximizing expected return; they require principled uncertainty management.

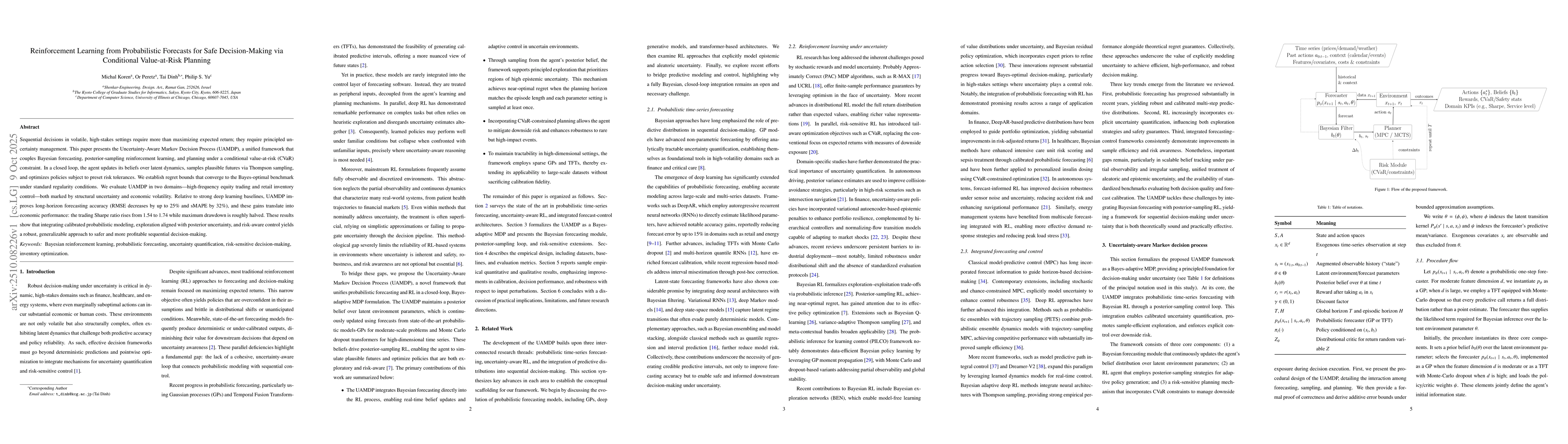

This paper presents the Uncertainty-Aware Markov Decision Process (UAMDP), a

unified framework that couples Bayesian forecasting, posterior-sampling

reinforcement learning, and planning under a conditional value-at-risk (CVaR)

constraint. In a closed loop, the agent updates its beliefs over latent

dynamics, samples plausible futures via Thompson sampling, and optimizes

policies subject to preset risk tolerances. We establish regret bounds that

converge to the Bayes-optimal benchmark under standard regularity conditions.

We evaluate UAMDP in two domains-high-frequency equity trading and retail

inventory control-both marked by structural uncertainty and economic

volatility. Relative to strong deep learning baselines, UAMDP improves

long-horizon forecasting accuracy (RMSE decreases by up to 25\% and sMAPE by

32\%), and these gains translate into economic performance: the trading Sharpe

ratio rises from 1.54 to 1.74 while maximum drawdown is roughly halved. These

results show that integrating calibrated probabilistic modeling, exploration

aligned with posterior uncertainty, and risk-aware control yields a robust,

generalizable approach to safer and more profitable sequential decision-making.

Discussion 0