Publication

Metrics

AI Quick Summary

This paper explores risk-averse multi-armed bandit problems using the mean-variance measure, demonstrating lower bounds on model-specific and model-independent regret in $\Omega(\log T)$ and $\Omega(T^{2/3})$, respectively. It adapts the UCB and DSEE policies to achieve these bounds, extending classic risk-neutral bandit models into a risk-aware framework.

Paper Preview

Abstract

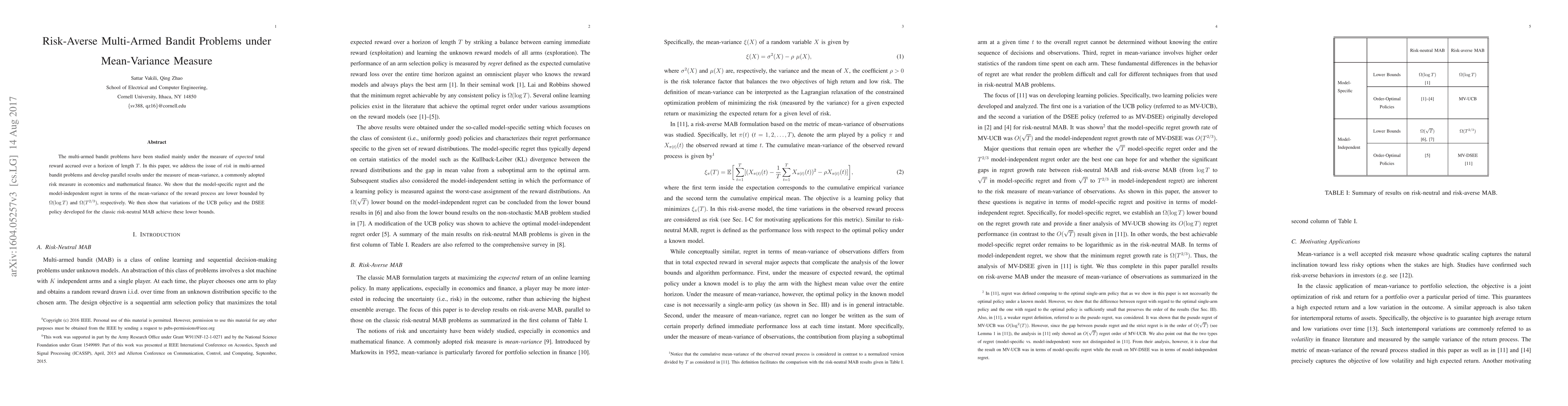

The multi-armed bandit problems have been studied mainly under the measure of expected total reward accrued over a horizon of length $T$. In this paper, we address the issue of risk in multi-armed bandit problems and develop parallel results under the measure of mean-variance, a commonly adopted risk measure in economics and mathematical finance. We show that the model-specific regret and the model-independent regret in terms of the mean-variance of the reward process are lower bounded by $\Omega(\log T)$ and $\Omega(T^{2/3})$, respectively. We then show that variations of the UCB policy and the DSEE policy developed for the classic risk-neutral MAB achieve these lower bounds.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0