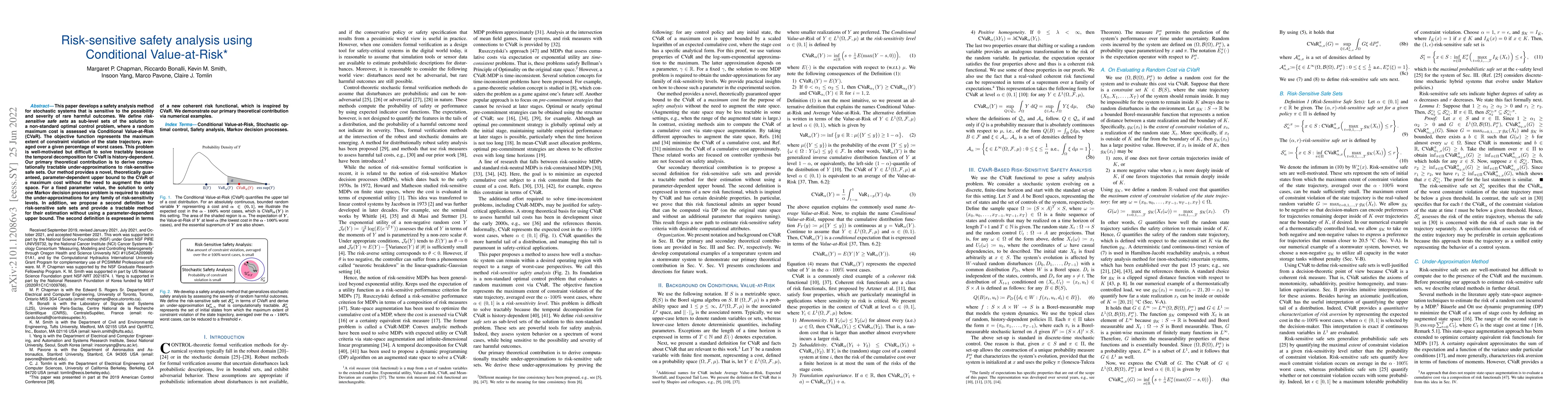

Risk-sensitive safety analysis using Conditional Value-at-Risk

Publication

Metrics

AI Quick Summary

This paper introduces a risk-sensitive safety analysis method for stochastic systems using Conditional Value-at-Risk (CVaR) to assess rare harmful outcomes. It proposes computationally tractable under-approximations for risk-sensitive safe sets, requiring only one Markov decision process solution for any risk-sensitivity level.

Paper Preview

Abstract

This paper develops a safety analysis method for stochastic systems that is sensitive to the possibility and severity of rare harmful outcomes. We define risk-sensitive safe sets as sub-level sets of the solution to a non-standard optimal control problem, where a random maximum cost is assessed via Conditional Value-at-Risk (CVaR). The objective function represents the maximum extent of constraint violation of the state trajectory, averaged over a given percentage of worst cases. This problem is well-motivated but difficult to solve tractably because the temporal decomposition for CVaR is history-dependent. Our primary theoretical contribution is to derive computationally tractable under-approximations to risk-sensitive safe sets. Our method provides a novel, theoretically guaranteed, parameter-dependent upper bound to the CVaR of a maximum cost without the need to augment the state space. For a fixed parameter value, the solution to only one Markov decision process problem is required to obtain the under-approximations for any family of risk-sensitivity levels. In addition, we propose a second definition for risk-sensitive safe sets and provide a tractable method for their estimation without using a parameter-dependent upper bound. The second definition is expressed in terms of a new coherent risk functional, which is inspired by CVaR. We demonstrate our primary theoretical contribution via numerical examples.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0