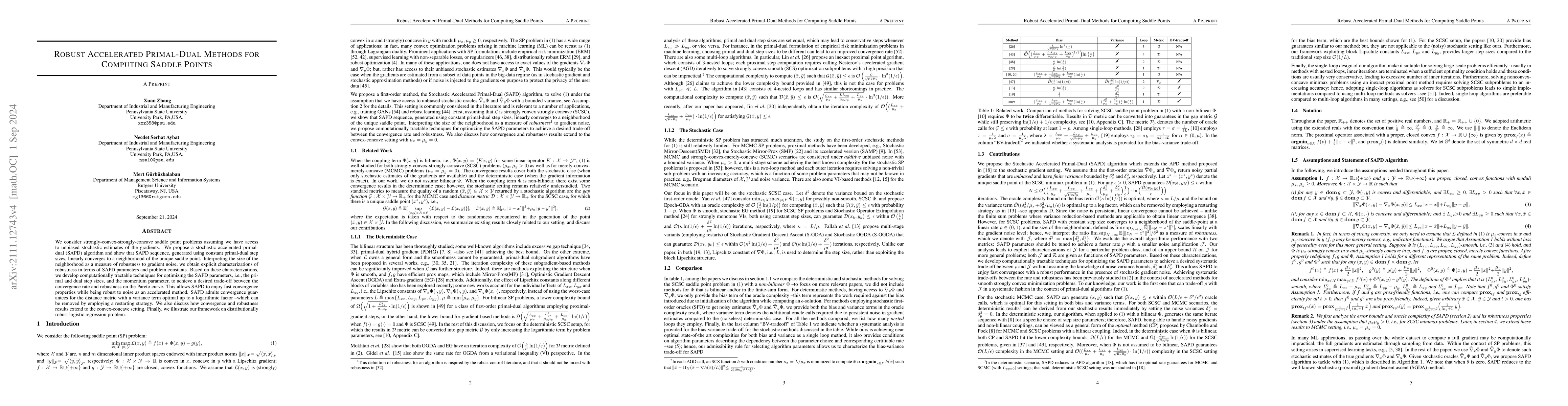

Robust Accelerated Primal-Dual Methods for Computing Saddle Points

Publication

Metrics

AI Quick Summary

This paper proposes a stochastic accelerated primal-dual (SAPD) algorithm for solving strongly-convex-strongly-concave saddle point problems, demonstrating linear convergence to a neighborhood of the saddle point. The authors optimize SAPD parameters to balance convergence speed and robustness to gradient noise, achieving optimal convergence guarantees with a variance term.

Paper Preview

Abstract

We consider strongly-convex-strongly-concave saddle point problems assuming we have access to unbiased stochastic estimates of the gradients. We propose a stochastic accelerated primal-dual (SAPD) algorithm and show that SAPD sequence, generated using constant primal-dual step sizes, linearly converges to a neighborhood of the unique saddle point. Interpreting the size of the neighborhood as a measure of robustness to gradient noise, we obtain explicit characterizations of robustness in terms of SAPD parameters and problem constants. Based on these characterizations, we develop computationally tractable techniques for optimizing the SAPD parameters, i.e., the primal and dual step sizes, and the momentum parameter, to achieve a desired trade-off between the convergence rate and robustness on the Pareto curve. This allows SAPD to enjoy fast convergence properties while being robust to noise as an accelerated method. SAPD admits convergence guarantees for the distance metric with a variance term optimal up to a logarithmic factor, which can be removed by employing a restarting strategy. We also discuss how convergence and robustness results extend to the convex-concave setting. Finally, we illustrate our framework on distributionally robust logistic regression.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0