The study develops a robust hedging valuation adjustment (HVA) framework by simulating rebalancing and maturity-unwind trades to generate loss distributions for no-trade-band rules, and then defining robust HVA as the worst-case expected loss over a relative-entropy neighborhood. It compares fixed-radius versus fixed benchmark-stress conventions, and uses KL-based robustification with loss-samples and optimization to derive robust upper-HVA and corresponding weights. The methodology includes two processing conventions (fixed-radius and benchmark-stress) and three algorithms for loss-sample generation, KL upper bound computation, and map construction between radius/stress and outcomes, with explicit treatment of turnover, hedge-error risk, and band-dependent effects.

Robust Hedging Valuation Adjustment under Liquidity--Demand Stress

Publication

Metrics

Quick Answers

What methodology did the authors use?

The study develops a robust hedging valuation adjustment (HVA) framework by simulating rebalancing and maturity-unwind trades to generate loss distributions for no-trade-band rules, and then defining robust HVA as the worst-case expected loss over a relative-entropy neighborhood. It compares fixed-radius versus fixed benchmark-stress conventions, and uses KL-based robustification with loss-samples and optimization to derive robust upper-HVA and corresponding weights. The... More in Methodology →

What are the key results?

Under fixed-radius and benchmark-stress conventions, robust HVAs yield similar values in high-liquidity regimes but diverge when liquidity is stressed, indicating convention sensitivity to market conditions. — Wider no-trade bands reduce rebalancing costs but increase hedge-error risk, highlighting a trade-off between turnover and hedging accuracy. More in Key Results →

Why is this work significant?

The paper introduces a tractable, entropy-based robust framework for hedging valuation adjustments that explicitly accounts for liquidity-demand stress and turnover differences across hedging policies, facilitating more resilient pricing under market frictions. More in Significance →

What are the main limitations?

Reliance on simulated rebalancing paths may not capture all real-world liquidity regimes or model misspecification in stress scenarios. — Assumptions on the two-state normal–stress specification and baseline half-spread may limit generalizability to more complex market microstructures. More in Limitations →

Paper Preview

Abstract

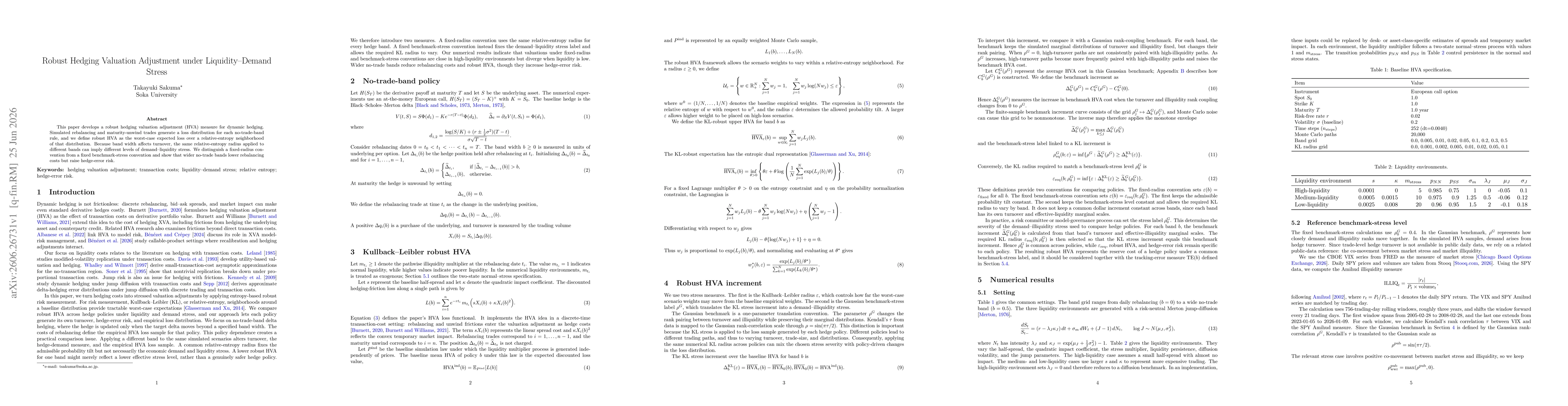

This paper develops a robust hedging valuation adjustment (HVA) measure for dynamic hedging. Simulated rebalancing and maturity-unwind trades generate a loss distribution for each no-trade-band rule, and we define robust HVA as the worst-case expected loss over a relative-entropy neighborhood of that distribution. Because band width affects turnover, the same relative-entropy radius applied to different bands can imply different levels of demand-liquidity stress. We distinguish a fixed-radius convention from a fixed benchmark-stress convention and show that wider no-trade bands lower rebalancing costs but raise hedge-error risk.

Key Findings, in focus

Seven facets of this paper, analysed and brought into focus by AI.

The paper introduces a tractable, entropy-based robust framework for hedging valuation adjustments that explicitly accounts for liquidity-demand stress and turnover differences across hedging policies, facilitating more resilient pricing under market frictions.

- Under fixed-radius and benchmark-stress conventions, robust HVAs yield similar values in high-liquidity regimes but diverge when liquidity is stressed, indicating convention sensitivity to market conditions.

- Wider no-trade bands reduce rebalancing costs but increase hedge-error risk, highlighting a trade-off between turnover and hedging accuracy.

- KL-based robustification provides tractable worst-case expectations and probabilistic weights, enabling explicit comparison across hedge policies with differing turnover profiles.

The paper introduces a tractable, entropy-based robust framework for hedging valuation adjustments that explicitly accounts for liquidity-demand stress and turnover differences across hedging policies, facilitating more resilient pricing under market frictions.

Proposes a discrete-time robust HVA framework with explicit loss function L(b), incorporating turnover costs and market impact, and develops algorithms to (i) generate loss samples under maturity unwind, (ii) compute KL-based robust upper HVAs with optimal weights, and (iii) map fixed-radius and fixed-stress conventions to benchmark stress levels via monotone envelopes.

First integration of relative-entropy robustification into hedging valuation adjustment under liquidity-demand stress, with a systematic comparison of fixed-radius and fixed-benchmark conventions and explicit treatment of turnover-induced differences in risk and cost.

- Reliance on simulated rebalancing paths may not capture all real-world liquidity regimes or model misspecification in stress scenarios.

- Assumptions on the two-state normal–stress specification and baseline half-spread may limit generalizability to more complex market microstructures.

- Computational complexity could rise with finer grids for radius and stress, potentially challenging real-time risk reporting.

- Extend to multi-asset hedges and path-dependent derivatives to assess robustness in higher dimensions.

- Explore alternative risk measures beyond KL divergence (e.g., Wasserstein) to gauge sensitivity to distributional assumptions.

- Empirically validate the fixed-radius versus fixed-benchmark conventions using live market data across diverse liquidity environments.

Discussion 0