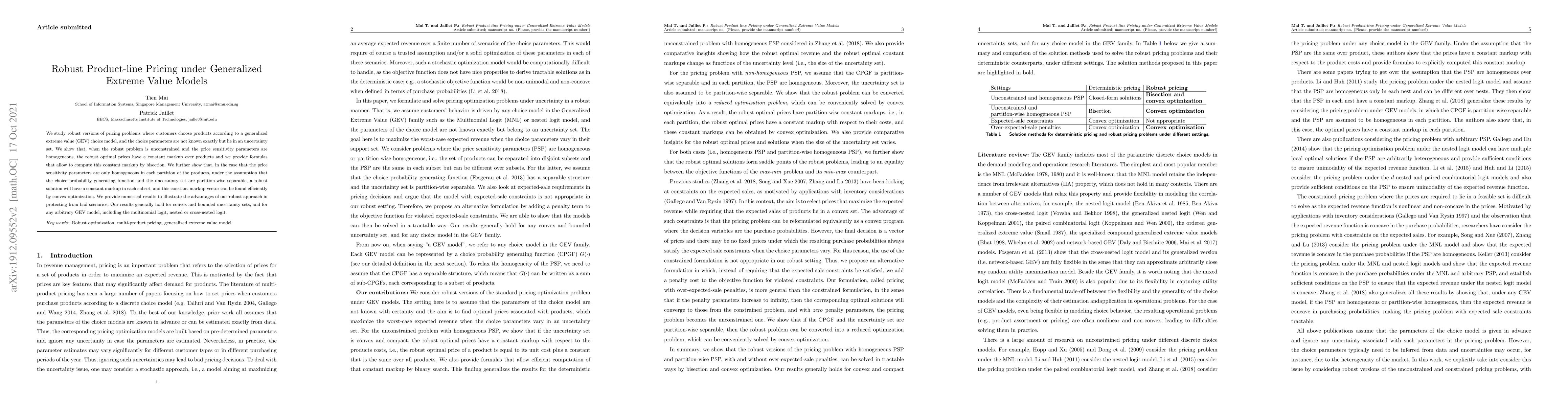

We study robust versions of pricing problems where customers choose products

according to a generalized extreme value (GEV) choice model, and the choice

parameters are not known exactly but lie in an uncertainty set. We show that,

when the robust problem is unconstrained and the price sensitivity parameters

are homogeneous, the robust optimal prices have a constant markup over

products, and we provide formulas that allow to compute this constant markup by

bisection. We further show that, in the case that the price sensitivity

parameters are only homogeneous in each partition of the products, under the

assumption that the choice probability generating function and the uncertainty

set are partition-wise separable, a robust solution will have a constant markup

in each subset, and this constant-markup vector can be found efficiently by

convex optimization. We provide numerical results to illustrate the advantages

of our robust approach in protecting from bad scenarios. Our results hold for

convex and bounded uncertainty sets,} and for any arbitrary GEV model,

including the multinomial logit, nested or cross-nested logit.

Discussion 0