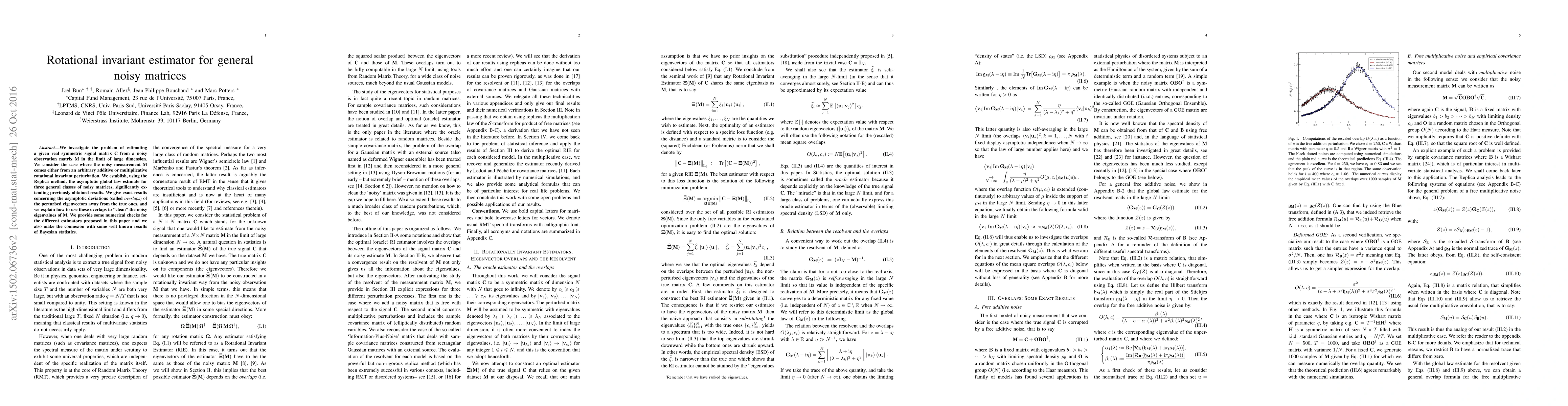

Publication

Metrics

AI Quick Summary

This paper presents a rotational invariant estimator for real symmetric signal matrices $\textbf{C}$ observed through noisy matrices $\textbf{M}$, considering both additive and multiplicative perturbations. It uses the Replica method to derive asymptotic global law estimates for three classes of noisy matrices, providing exact results for perturbed eigenvectors and a method to clean noisy eigenvalues.

Paper Preview

Abstract

We investigate the problem of estimating a given real symmetric signal matrix $\textbf{C}$ from a noisy observation matrix $\textbf{M}$ in the limit of large dimension. We consider the case where the noisy measurement $\textbf{M}$ comes either from an arbitrary additive or multiplicative rotational invariant perturbation. We establish, using the Replica method, the asymptotic global law estimate for three general classes of noisy matrices, significantly extending previously obtained results. We give exact results concerning the asymptotic deviations (called overlaps) of the perturbed eigenvectors away from the true ones, and we explain how to use these overlaps to "clean" the noisy eigenvalues of $\textbf{M}$. We provide some numerical checks for the different estimators proposed in this paper and we also make the connection with some well known results of Bayesian statistics.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0