Scaling and memory in the non-poisson process of limit order cancelation

Publication

Metrics

Paper Preview

Abstract

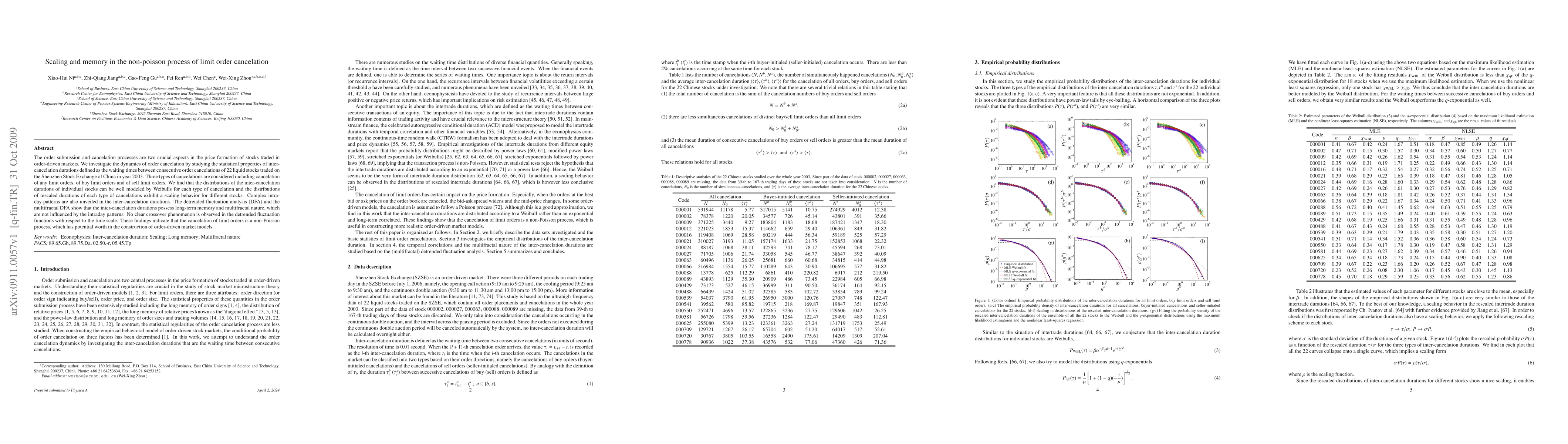

The order submission and cancelation processes are two crucial aspects in the price formation of stocks traded in order-driven markets. We investigate the dynamics of order cancelation by studying the statistical properties of inter-cancelation durations defined as the waiting times between consecutive order cancelations of 22 liquid stocks traded on the Shenzhen Stock Exchange of China in year 2003. Three types of cancelations are considered including cancelation of any limit orders, of buy limit orders and of sell limit orders. We find that the distributions of the inter-cancelation durations of individual stocks can be well modeled by Weibulls for each type of cancelation and the distributions of rescaled durations of each type of cancelations exhibit a scaling behavior for different stocks. Complex intraday patterns are also unveiled in the inter-cancelation durations. The detrended fluctuation analysis (DFA) and the multifractal DFA show that the inter-cancelation durations possess long-term memory and multifractal nature, which are not influenced by the intraday patterns. No clear crossover phenomenon is observed in the detrended fluctuation functions with respect to the time scale. These findings indicate that the cancelation of limit orders is a non-Poisson process, which has potential worth in the construction of order-driven market models.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0