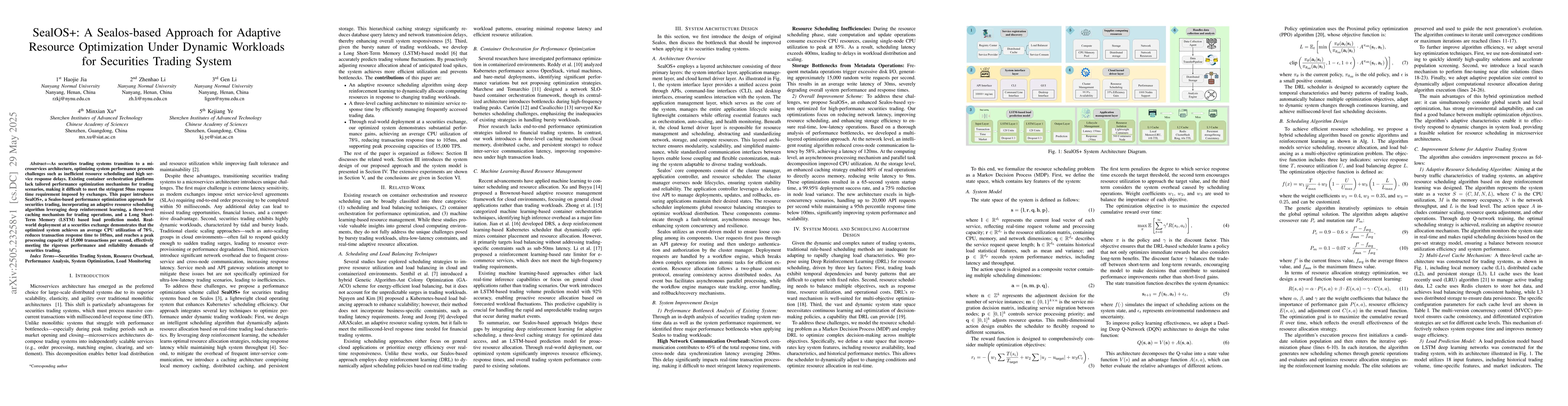

As securities trading systems transition to a microservices architecture,

optimizing system performance presents challenges such as inefficient resource

scheduling and high service response delays. Existing container orchestration

platforms lack tailored performance optimization mechanisms for trading

scenarios, making it difficult to meet the stringent 50ms response time

requirement imposed by exchanges. This paper introduces SealOS+, a Sealos-based

performance optimization approach for securities trading, incorporating an

adaptive resource scheduling algorithm leveraging deep reinforcement learning,

a three-level caching mechanism for trading operations, and a Long Short-Term

Memory (LSTM) based load prediction model. Real-world deployment at a

securities exchange demonstrates that the optimized system achieves an average

CPU utilization of 78\%, reduces transaction response time to 105ms, and

reaches a peak processing capacity of 15,000 transactions per second,

effectively meeting the rigorous performance and reliability demands of

securities trading.

Discussion 0