Multi-type Markov point processes offer a flexible framework for modelling

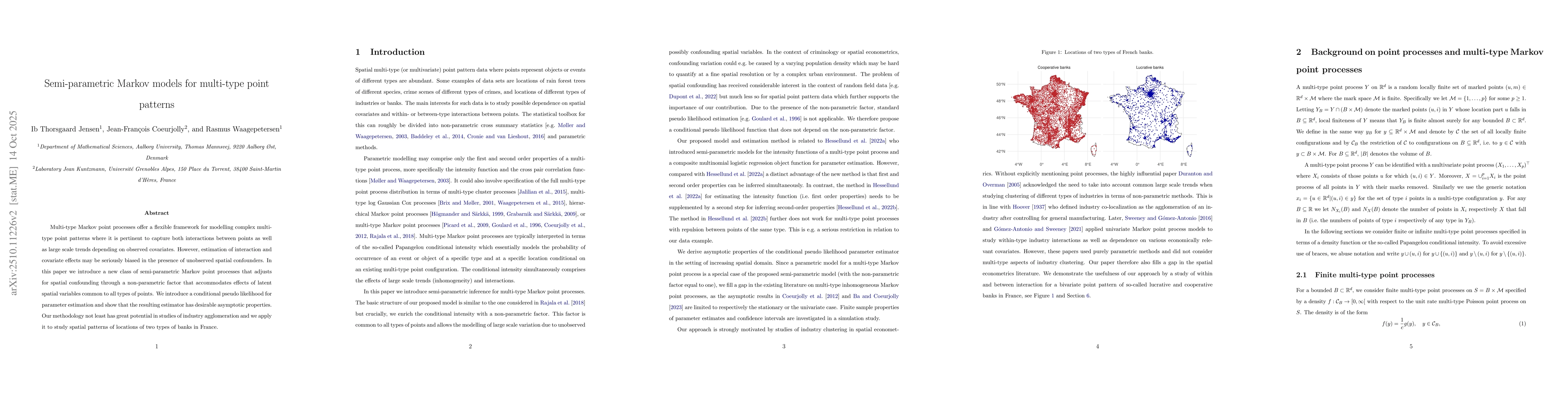

complex multi-type point patterns where it is pertinent to capture both

interactions between points as well as large scale trends depending on observed

covariates. However, estimation of interaction and covariate effects may be

seriously biased in the presence of unobserved spatial confounders. In this

paper we introduce a new class of semi-parametric Markov point processes that

adjusts for spatial confounding through a non-parametric factor that

accommodates effects of latent spatial variables common to all types of points.

We introduce a conditional pseudo likelihood for parameter estimation and show

that the resulting estimator has desirable asymptotic properties. Our

methodology not least has great potential in studies of industry agglomeration

and we apply it to study spatial patterns of locations of two types of banks in

France.

Discussion 0