Sequential optimizing investing strategy with neural networks

Publication

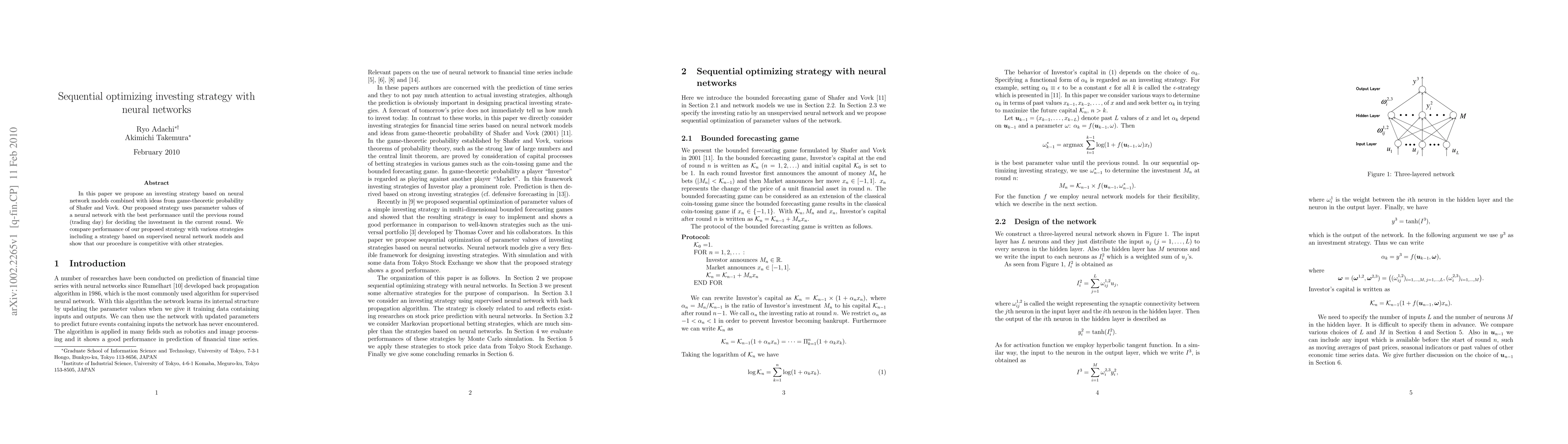

Metrics

Paper Preview

Abstract

In this paper we propose an investing strategy based on neural network models combined with ideas from game-theoretic probability of Shafer and Vovk. Our proposed strategy uses parameter values of a neural network with the best performance until the previous round (trading day) for deciding the investment in the current round. We compare performance of our proposed strategy with various strategies including a strategy based on supervised neural network models and show that our procedure is competitive with other strategies.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0