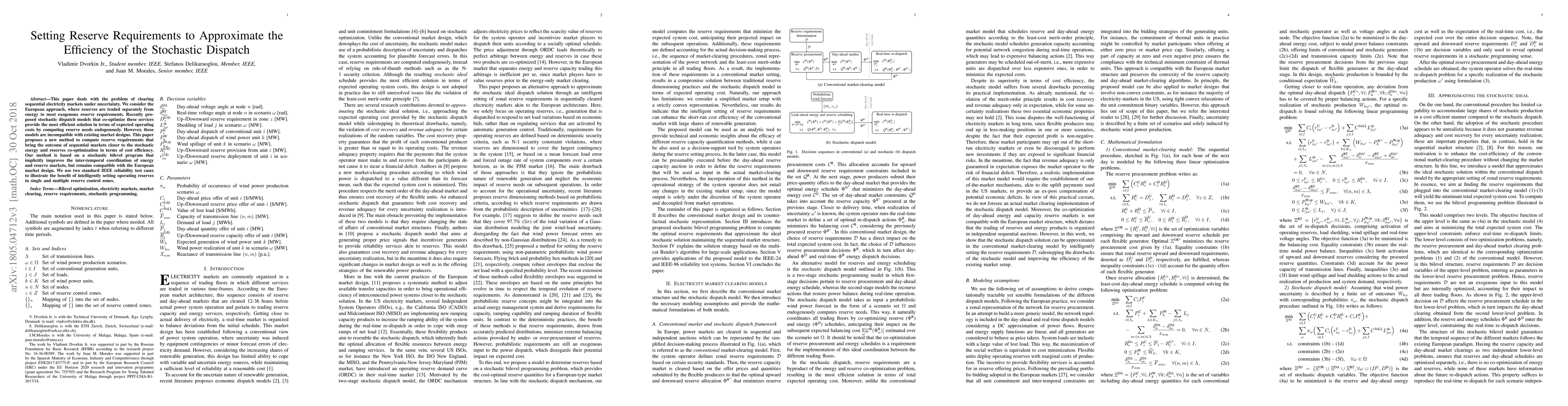

Setting Reserve Requirements to Approximate the Efficiency of the Stochastic Dispatch

Publication

Metrics

AI Quick Summary

This paper proposes a new method to compute reserve requirements in electricity markets that efficiently approximates stochastic dispatch outcomes while remaining compatible with existing market designs.

Paper Preview

Abstract

This paper deals with the problem of clearing sequential electricity markets under uncertainty. We consider the European approach, where reserves are traded separately from energy to meet exogenous reserve requirements. Recently pro- posed stochastic dispatch models that co-optimize these services provide the most efficient solution in terms of expected operating costs by computing reserve needs endogenously. However, these models are incompatible with existing market designs. This paper proposes a new method to compute reserve requirements that bring the outcome of sequential markets closer to the stochastic energy and reserves co-optimization in terms of cost efficiency. Our method is based on a stochastic bilevel program that implicitly improves the inter-temporal coordination of energy and reserve markets, but remains compatible with the European market design. We use two standard IEEE reliability test cases to illustrate the benefit of intelligently setting operating reserves in single and multiple reserve control zones.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0