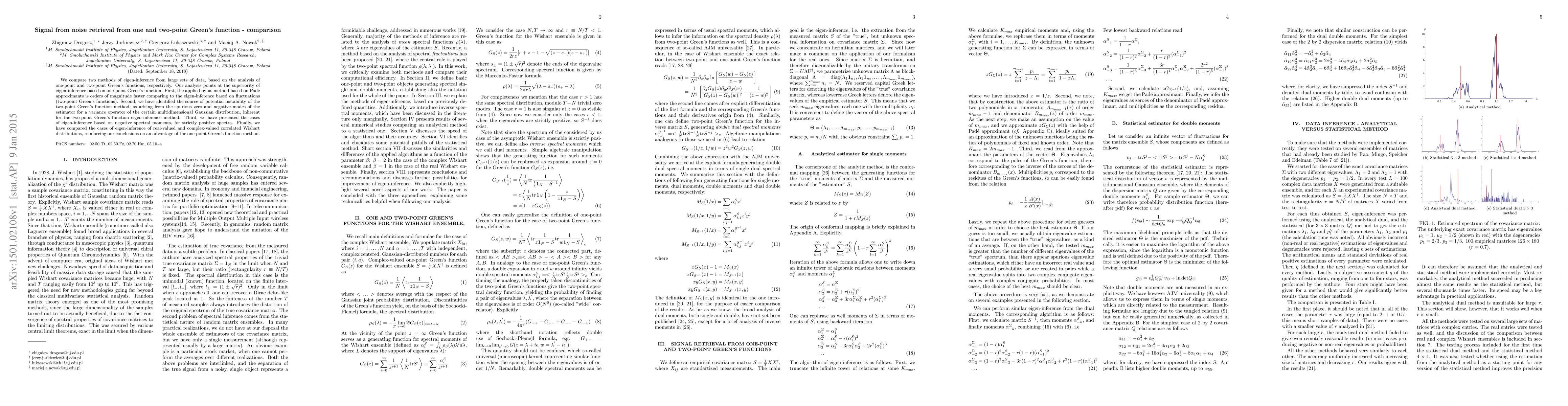

Signal from noise retrieval from one and two-point Green's function - comparison

Publication

Metrics

AI Quick Summary

The paper compares two eigen-inference methods from large datasets using one-point and two-point Green's functions. It highlights the superiority of the one-point method due to its speed and stability, identifying the two-point method's potential instability from spurious zero and negative modes. The research also explores eigen-inference based on negative spectral moments and compares real-valued and complex-valued correlated Wishart distributions, supporting the one-point Green's function method's advantage.

Paper Preview

Abstract

We compare two methods of eigen-inference from large sets of data, based on the analysis of one-point and two-point Green's functions, respectively. Our analysis points at the superiority of eigen-inference based on one-point Green's function. First, the applied by us method based on Pad?e approximants is orders of magnitude faster comparing to the eigen-inference based on uctuations (two-point Green's functions). Second, we have identified the source of potential instability of the two-point Green's function method, as arising from the spurious zero and negative modes of the estimator for a variance operator of the certain multidimensional Gaussian distribution, inherent for the two-point Green's function eigen-inference method. Third, we have presented the cases of eigen-inference based on negative spectral moments, for strictly positive spectra. Finally, we have compared the cases of eigen-inference of real-valued and complex-valued correlated Wishart distributions, reinforcing our conclusions on an advantage of the one-point Green's function method.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0