Publication

Metrics

AI Quick Summary

This paper critiques Bulgaria's existing revenue forecasting models, finding they underperform expectations based on the 'Laffer curve'. It proposes transparent, implementable alternatives that outperform current models in predicting personal- and corporate-income tax revenues.

Paper Preview

Abstract

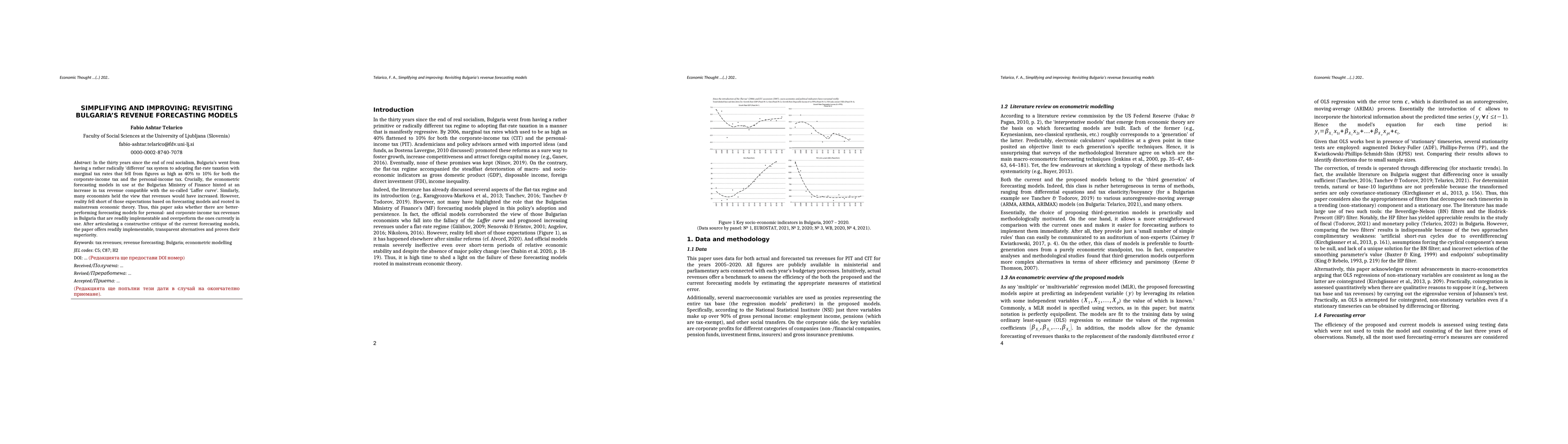

In the thirty years since the end of real socialism, Bulgaria's went from having a rather radically 'different' tax system to adopting flat-rate taxation with marginal tax rates that fell from figures as high as 40% to 10% for both the corporate-income tax and the personal-income tax. Crucially, the econometric forecasting models in use at the Bulgarian Ministry of Finance hinted at an increase in tax revenue compatible with the so-called 'Laffer curve'. Similarly, many economists held the view that revenues would have increased. However, reality fell short of those expectations based on forecasting models and rooted in mainstream economic theory. Thus, this paper asks whether there are betterperforming forecasting models for personal-and corporate-income tax-revenues in Bulgaria that are readily implementable and overperform the ones currently in use. After articulating a constructive critique of the current forecasting models, the paper offers readily implementable, transparent alternatives and proves their superiority.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0