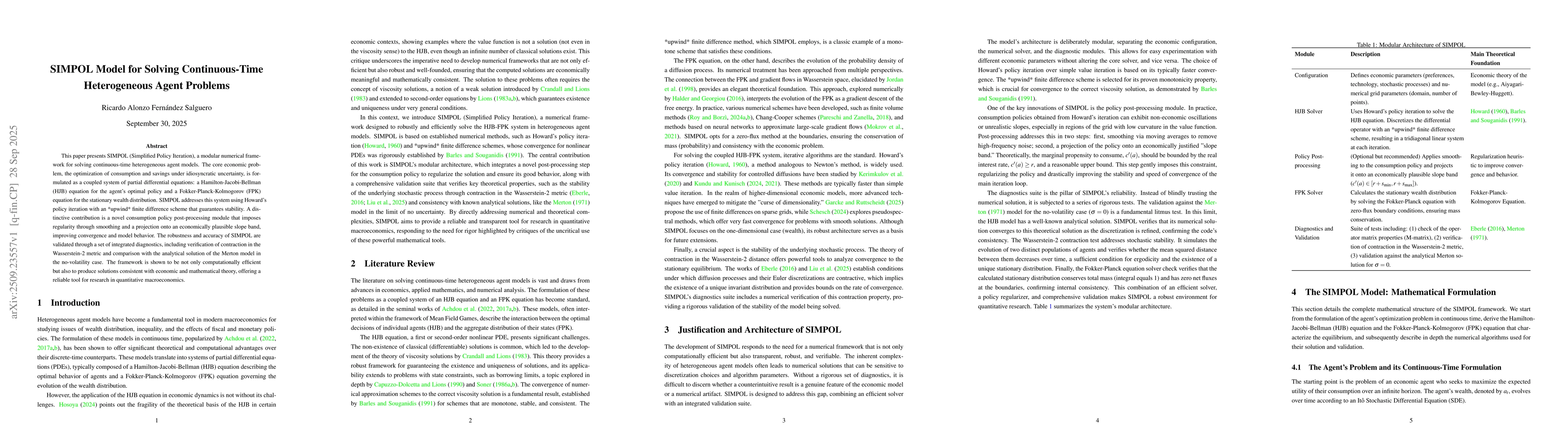

This paper presents SIMPOL (Simplified Policy Iteration), a modular numerical

framework for solving continuous-time heterogeneous agent models. The core

economic problem, the optimization of consumption and savings under

idiosyncratic uncertainty, is formulated as a coupled system of partial

differential equations: a Hamilton-Jacobi-Bellman (HJB) equation for the

agent's optimal policy and a Fokker-Planck-Kolmogorov (FPK) equation for the

stationary wealth distribution. SIMPOL addresses this system using Howard's

policy iteration with an *upwind* finite difference scheme that guarantees

stability. A distinctive contribution is a novel consumption policy

post-processing module that imposes regularity through smoothing and a

projection onto an economically plausible slope band, improving convergence and

model behavior. The robustness and accuracy of SIMPOL are validated through a

set of integrated diagnostics, including verification of contraction in the

Wasserstein-2 metric and comparison with the analytical solution of the Merton

model in the no-volatility case. The framework is shown to be not only

computationally efficient but also to produce solutions consistent with

economic and mathematical theory, offering a reliable tool for research in

quantitative macroeconomics.

Discussion 0