Manufacturing quality audits are pivotal for ensuring high product standards

in mass production environments. Traditional auditing processes, however, are

labor-intensive and reliant on human expertise, posing challenges in

maintaining transparency, accountability, and continuous improvement across

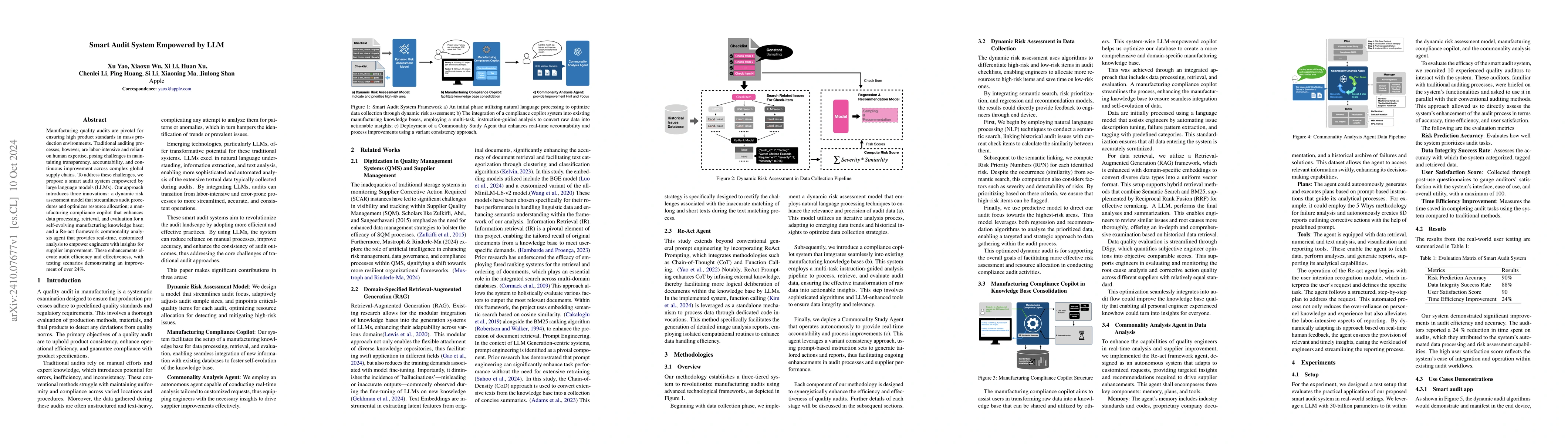

complex global supply chains. To address these challenges, we propose a smart

audit system empowered by large language models (LLMs). Our approach introduces

three innovations: a dynamic risk assessment model that streamlines audit

procedures and optimizes resource allocation; a manufacturing compliance

copilot that enhances data processing, retrieval, and evaluation for a

self-evolving manufacturing knowledge base; and a Re-act framework commonality

analysis agent that provides real-time, customized analysis to empower

engineers with insights for supplier improvement. These enhancements elevate

audit efficiency and effectiveness, with testing scenarios demonstrating an

improvement of over 24%.

Discussion 0