Publication

Metrics

AI Quick Summary

This paper introduces a smoothed quantile regression method called "conquer" for large-scale data with increasing dimensions. It transforms the non-differentiable quantile loss into a differentiable surrogate, enabling scalable optimization and statistical inference via multiplier bootstrap. Theoretical and empirical results validate the method's efficiency and accuracy.

Paper Preview

Abstract

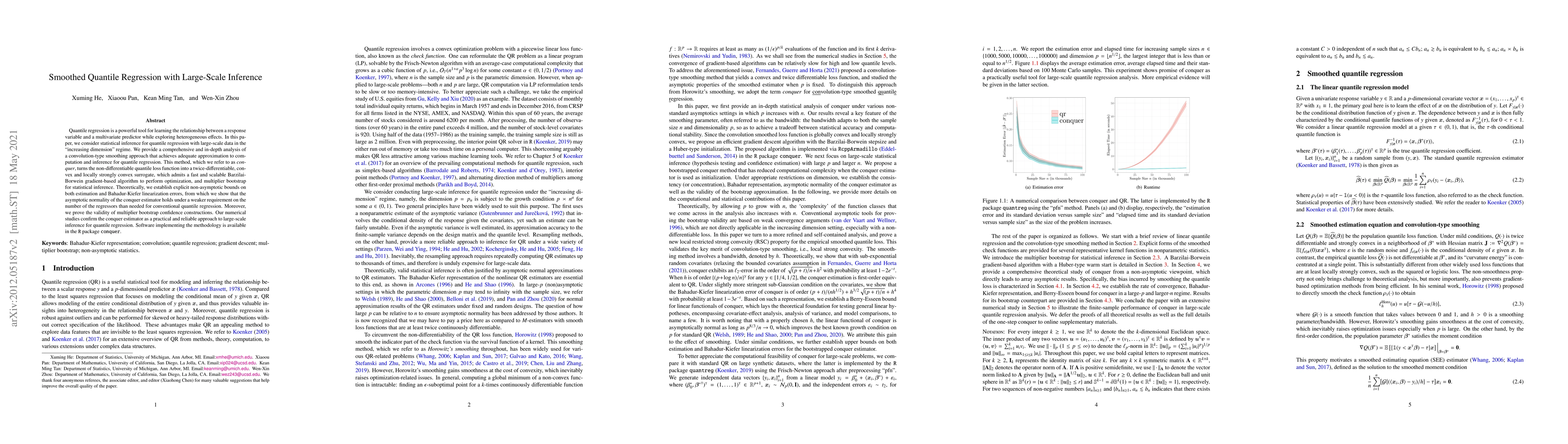

Quantile regression is a powerful tool for learning the relationship between a response variable and a multivariate predictor while exploring heterogeneous effects. In this paper, we consider statistical inference for quantile regression with large-scale data in the "increasing dimension" regime. We provide a comprehensive and in-depth analysis of a convolution-type smoothing approach that achieves adequate approximation to computation and inference for quantile regression. This method, which we refer to as {\it{conquer}}, turns the non-differentiable quantile loss function into a twice-differentiable, convex and locally strongly convex surrogate, which admits a fast and scalable Barzilai-Borwein gradient-based algorithm to perform optimization, and multiplier bootstrap for statistical inference. Theoretically, we establish explicit non-asymptotic bounds on both estimation and Bahadur-Kiefer linearization errors, from which we show that the asymptotic normality of the conquer estimator holds under a weaker requirement on the number of the regressors than needed for conventional quantile regression. Moreover, we prove the validity of multiplier bootstrap confidence constructions. Our numerical studies confirm the conquer estimator as a practical and reliable approach to large-scale inference for quantile regression. Software implementing the methodology is available in the \texttt{R} package \texttt{conquer}.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0