Publication

Metrics

AI Quick Summary

This paper proposes a penalized estimating method for sparse factor models to accurately estimate the variance-covariance matrix, demonstrating oracle properties and consistency even when the number of parameters grows. The method's effectiveness is validated through simulations and applied to portfolio allocation.

Paper Preview

Abstract

We consider the estimation of factor model-based variance-covariance matrix when the factor loading matrix is assumed sparse. To do so, we rely on a system of penalized estimating functions to account for the identification issue of the factor loading matrix while fostering sparsity in potentially all its entries. We prove the oracle property of the penalized estimator for the factor model when the dimension is fixed. That is, the penalization procedure can recover the true sparse support, and the estimator is asymptotically normally distributed. Consistency and recovery of the true zero entries are established when the number of parameters is diverging. These theoretical results are supported by simulation experiments, and the relevance of the proposed method is illustrated by an application to portfolio allocation.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

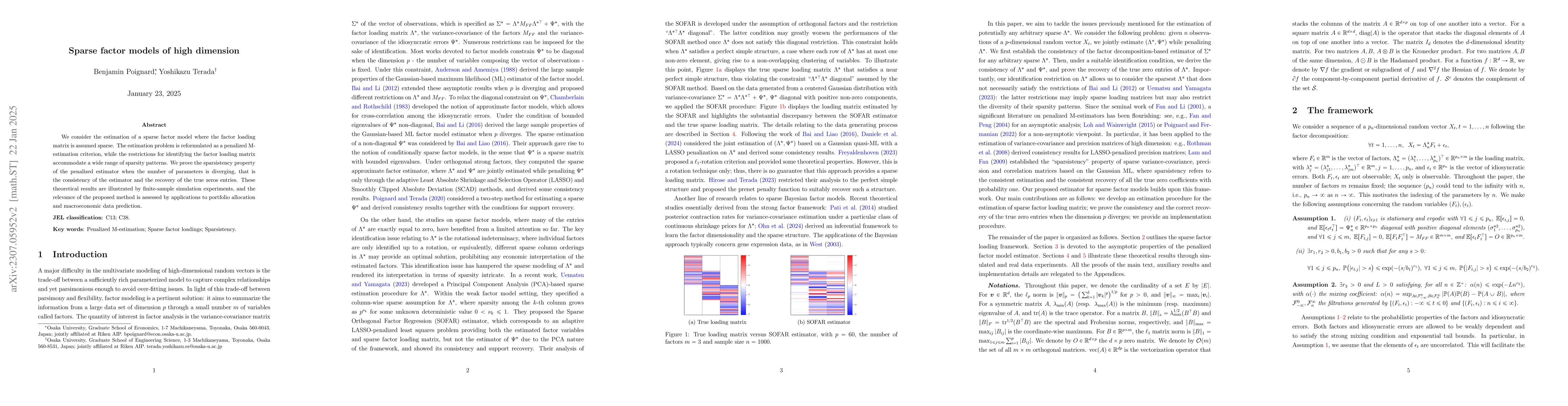

Discussion 0