Spatial Tweedie exponential dispersion models

Publication

Metrics

AI Quick Summary

This paper introduces a spatial Tweedie exponential dispersion model within a double generalized linear model framework, employing regularization and convex penalties to quantify uncertainty and spatial referencing. The proposed method, demonstrated via a coordinate descent algorithm, outperforms ridge and un-penalized versions in simulations, and is applied to model insurance losses from automobile collisions in Connecticut.

Paper Preview

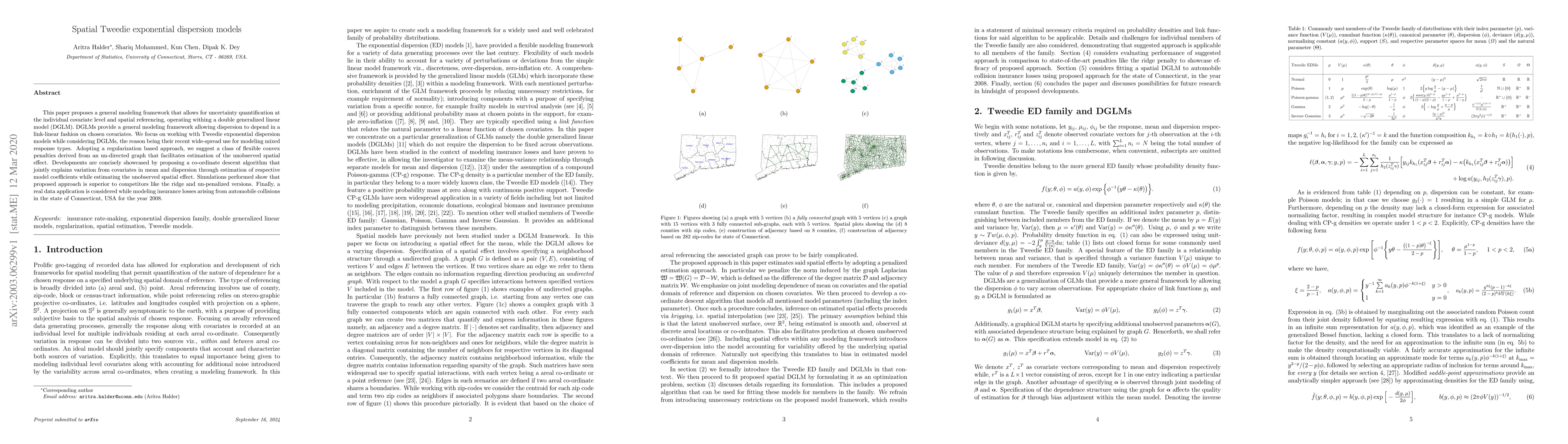

Abstract

This paper proposes a general modeling framework that allows for uncertainty quantification at the individual covariate level and spatial referencing, operating withing a double generalized linear model (DGLM). DGLMs provide a general modeling framework allowing dispersion to depend in a link-linear fashion on chosen covariates. We focus on working with Tweedie exponential dispersion models while considering DGLMs, the reason being their recent wide-spread use for modeling mixed response types. Adopting a regularization based approach, we suggest a class of flexible convex penalties derived from an un-directed graph that facilitates estimation of the unobserved spatial effect. Developments are concisely showcased by proposing a co-ordinate descent algorithm that jointly explains variation from covariates in mean and dispersion through estimation of respective model coefficients while estimating the unobserved spatial effect. Simulations performed show that proposed approach is superior to competitors like the ridge and un-penalized versions. Finally, a real data application is considered while modeling insurance losses arising from automobile collisions in the state of Connecticut, USA for the year 2008.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0