Spectral Adaptive Conformal Prediction for Structured Non-Exchangeable Data

Publication

Metrics

AI Quick Summary

The paper introduces spectral adaptive conformal prediction, a method that builds prediction intervals using locally weighted calibration residuals to handle non-exchangeable, structured time-series data. By updating the target miscoverage online and using spectral similarity to select relevant past errors, the approach can improve coverage accuracy in regimes with recurring patterns or changing frequencies, though its effectiveness depends on maintaining sufficient effective sample size.

Paper Preview

Abstract

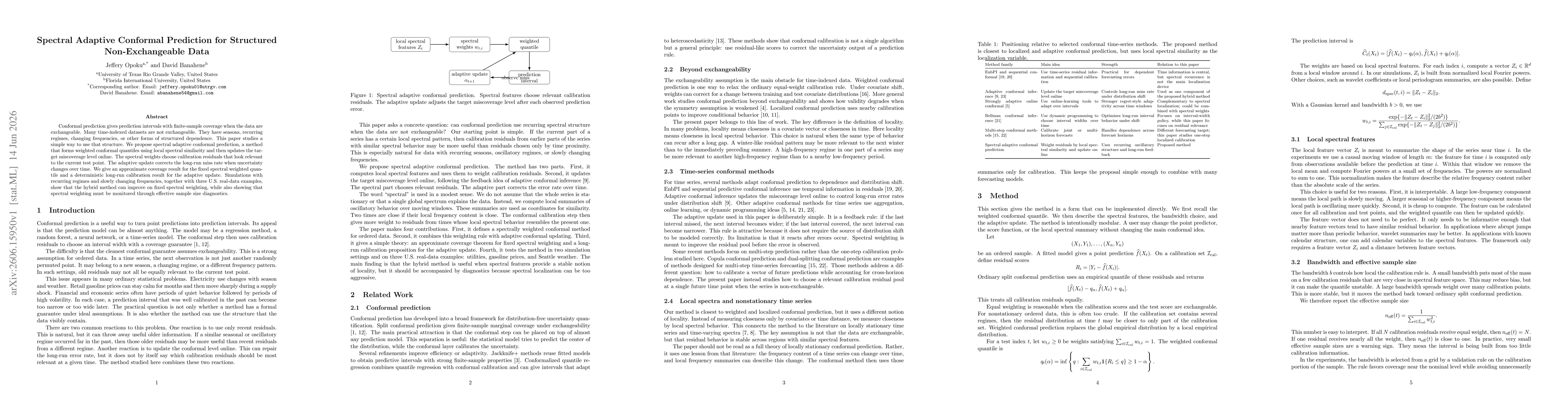

Conformal prediction gives prediction intervals with finite-sample coverage when the data are exchangeable. Many time-indexed datasets are not exchangeable. They have seasons, recurring regimes, changing frequencies, or other forms of structured dependence. This paper studies a simple way to use that structure. We propose spectral adaptive conformal prediction, a method that forms weighted conformal quantiles using local spectral similarity and then updates the target miscoverage level online. The spectral weights choose calibration residuals that look relevant to the current test point. The adaptive update corrects the long-run miss rate when uncertainty changes over time. We give an approximate coverage result for the fixed spectral weighted quantile and a deterministic long-run calibration result for the adaptive update. Simulations with recurring regimes and slowly changing frequencies, together with three U.S. real-data examples, show that the hybrid method can improve on fixed spectral weighting, while also showing that spectral weighting must be monitored through effective sample size diagnostics.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0