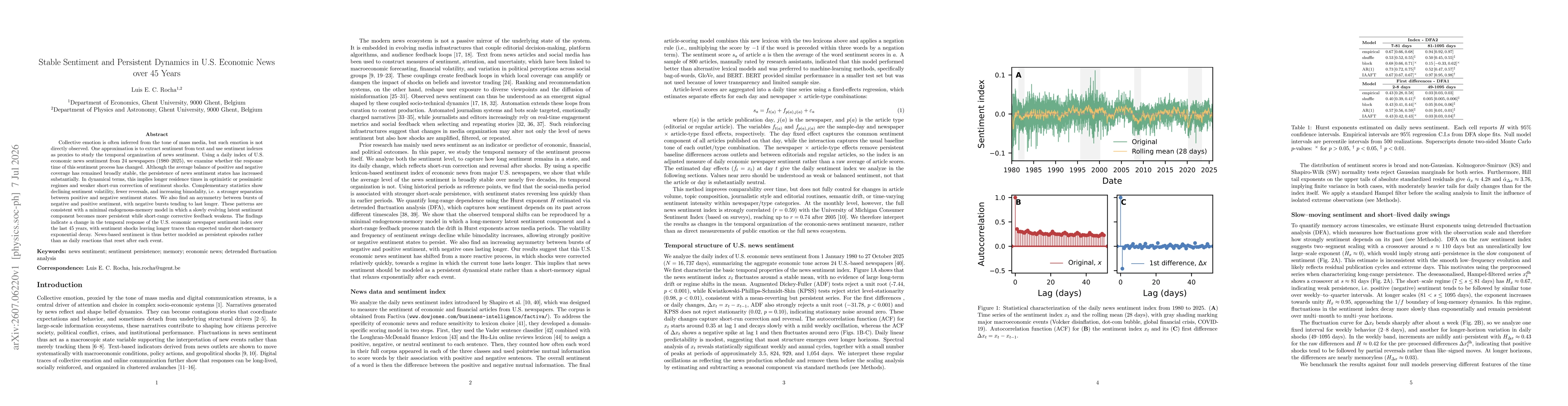

Collective emotion is often inferred from the tone of mass media, but such emotion is not directly observed. One approximation is to extract sentiment from text and use sentiment indexes as proxies to study the temporal organization of news sentiment. Using a daily index of U.S. economic news sentiment from 24 newspapers (1980-2025), we examine whether the response time of this sentiment process has changed. Although the average balance of positive and negative coverage has remained broadly stable, the persistence of news sentiment states has increased substantially. In dynamical terms, this implies longer residence times in optimistic or pessimistic regimes and weaker short-run correction of sentiment shocks. Complementary statistics show declining sentiment volatility, fewer reversals, and increasing bimodality, i.e. a stronger separation between positive and negative sentiment states. We also find an asymmetry between bursts of negative and positive sentiment, with negative bursts tending to last longer. These patterns are consistent with a minimal endogenous-memory model in which a slowly evolving latent sentiment component becomes more persistent while short-range corrective feedback weakens. The findings indicate a change in the temporal response of the U.S. economic newspaper sentiment index over the last 45 years, with sentiment shocks leaving longer traces than expected under short-memory exponential decay. News-based sentiment is thus better modeled as persistent episodes rather than as daily reactions that reset after each event.

Discussion 0