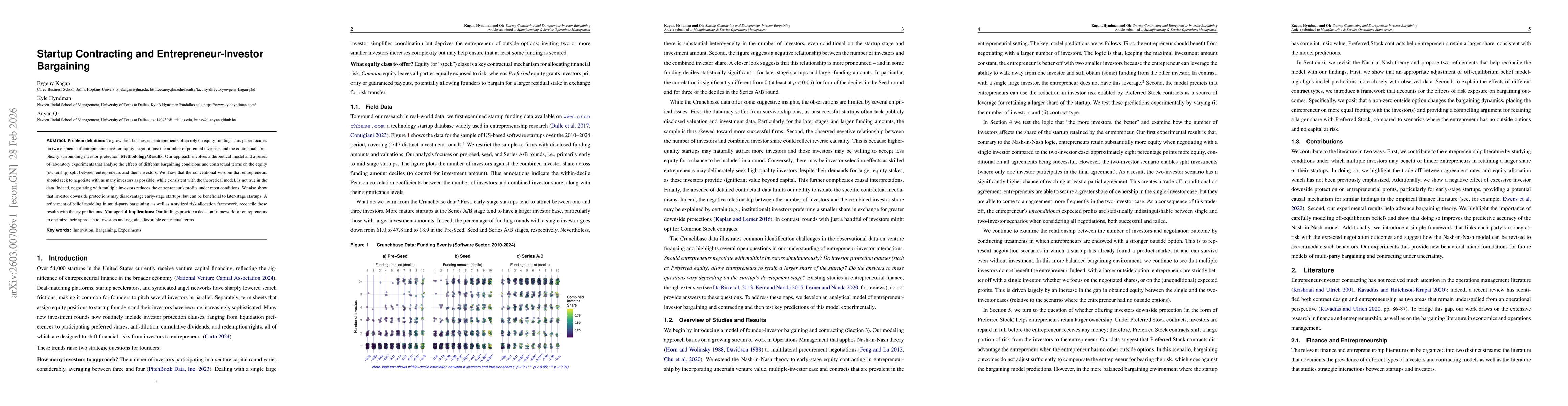

To grow their businesses, entrepreneurs often rely on equity funding. This paper focuses on two elements of entrepreneur-investor equity negotiations: the number of potential investors and the contractual complexity surrounding investor protection. Our approach involves a theoretical model and a series of laboratory experiments that analyze the effects of different bargaining conditions and contractual terms on the equity (ownership) split between entrepreneurs and their investors. We show that the conventional wisdom that entrepreneurs should seek to negotiate with as many investors as possible, while consistent with the theoretical model, is not true in the data. Indeed, negotiating with multiple investors reduces the entrepreneur's profits under most conditions. We also show that investor downside protections may disadvantage early-stage startups, but can be beneficial to later-stage startups. A refinement of belief modeling in multi-party bargaining, as well as a stylized risk allocation framework, reconcile these results with theory predictions. Our findings provide a decision framework for entrepreneurs to optimize their approach to investors and negotiate favorable contractual terms.

Discussion 0