Stationarity-Aware Retrieval-Augmented Time Series Forecasting

Publication

Metrics

AI Quick Summary

SARAF (Stationarity-Aware Retrieval-Augmented Time Series Forecasting) enhances time-series forecasting by retrieving past segments not just for similarity but with diversity to cover different regimes, and by adjusting how much diversity is used based on dataset stationarity. It then uses a stationarity-aware method to combine the retrieved futures, leading to stronger accuracy and robustness, especially in non-stationary settings, as demonstrated on eight real-world datasets.

Paper Preview

Abstract

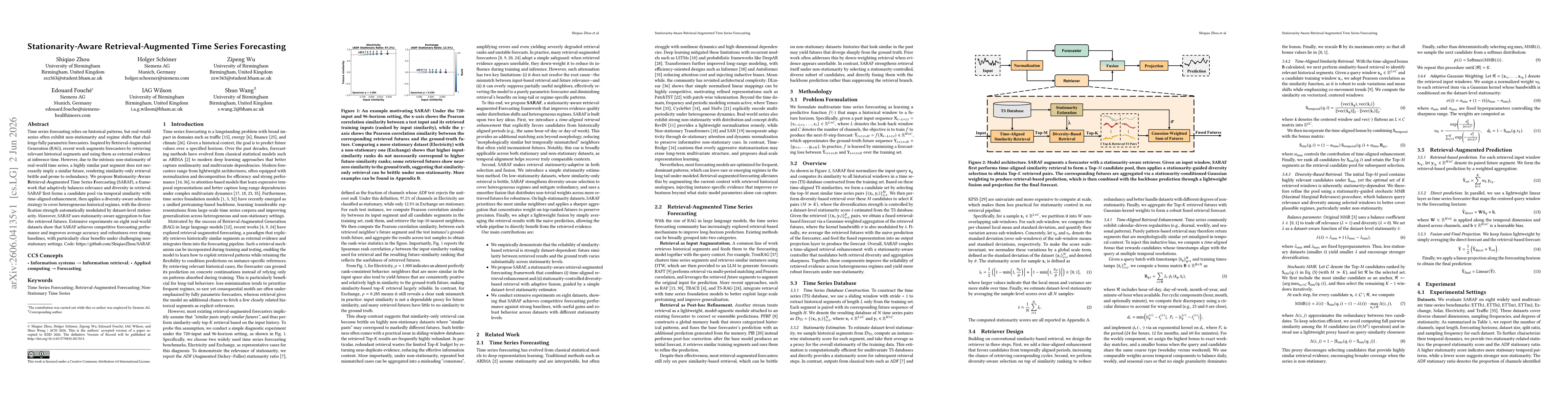

Time series forecasting relies on historical patterns, but real-world series often exhibit non-stationarity and regime shifts that challenge fully parametric forecasters. Inspired by Retrieval-Augmented Generation (RAG), recent work augments forecasters by retrieving relevant historical segments and using them as external evidence at inference time. However, due to the intrinsic non-stationarity of real-world time series, a highly similar past segment does not necessarily imply a similar future, rendering similarity-only retrieval brittle and prone to redundancy. We propose Stationarity-Aware Retrieval-Augmented Time Series Forecasting (SARAF), a framework that adaptively balances relevance and diversity in retrieval. SARAF first forms a candidate pool via temporal similarity with time-aligned enhancement, then applies a diversity-aware selection strategy to cover heterogeneous historical regimes, with the diversification strength automatically modulated by dataset-level stationarity. Moreover, SARAF uses stationarity-aware aggregation to fuse the retrieved futures. Extensive experiments on eight real-world datasets show that SARAF achieves competitive forecasting performance and improves average accuracy and robustness over strong baselines, with particularly clear benefits under challenging non-stationary settings. Code: https://github.com/ShiqiaoZhou/SARAF.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0