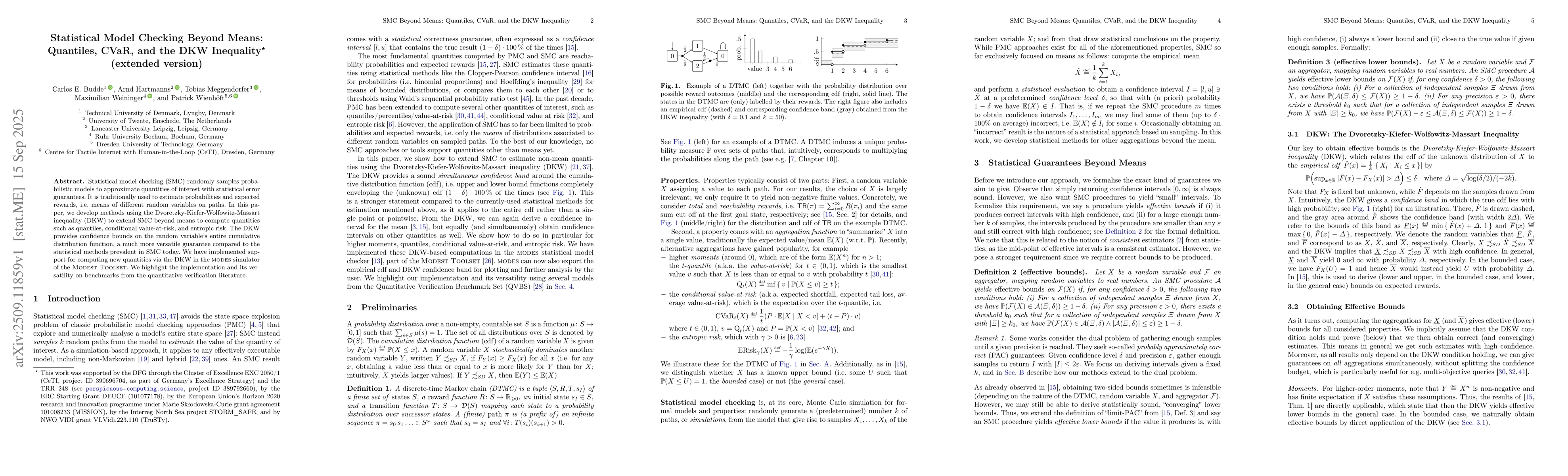

Statistical model checking (SMC) randomly samples probabilistic models to

approximate quantities of interest with statistical error guarantees. It is

traditionally used to estimate probabilities and expected rewards, i.e. means

of different random variables on paths. In this paper, we develop methods using

the Dvoretzky-Kiefer-Wolfowitz-Massart inequality (DKW) to extend SMC beyond

means to compute quantities such as quantiles, conditional value-at-risk, and

entropic risk. The DKW provides confidence bounds on the random variable's

entire cumulative distribution function, a much more versatile guarantee

compared to the statistical methods prevalent in SMC today. We have implemented

support for computing new quantities via the DKW in the 'modes' simulator of

the Modest Toolset. We highlight the implementation and its versatility on

benchmarks from the quantitative verification literature.

Discussion 0