Time series data often contain latent temporal structure, transitions between

locally stationary regimes, repeated motifs, and bursts of variability, that

are rarely leveraged in standard representation learning pipelines. Existing

models typically operate on raw or fixed-window sequences, treating all time

steps as equally informative, which leads to inefficiencies, poor robustness,

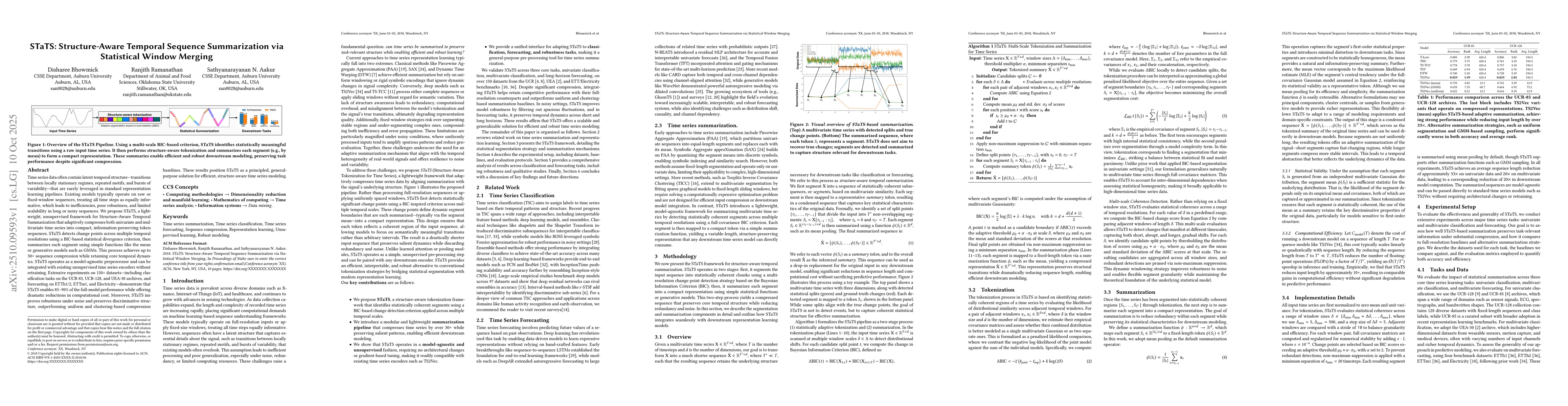

and limited scalability in long or noisy sequences. We propose STaTS, a

lightweight, unsupervised framework for Structure-Aware Temporal Summarization

that adaptively compresses both univariate and multivariate time series into

compact, information-preserving token sequences. STaTS detects change points

across multiple temporal resolutions using a BIC-based statistical divergence

criterion, then summarizes each segment using simple functions like the mean or

generative models such as GMMs. This process achieves up to 30x sequence

compression while retaining core temporal dynamics. STaTS operates as a

model-agnostic preprocessor and can be integrated with existing unsupervised

time series encoders without retraining. Extensive experiments on 150+

datasets, including classification tasks on the UCR-85, UCR-128, and UEA-30

archives, and forecasting on ETTh1 and ETTh2, ETTm1, and Electricity,

demonstrate that STaTS enables 85-90\% of the full-model performance while

offering dramatic reductions in computational cost. Moreover, STaTS improves

robustness under noise and preserves discriminative structure, outperforming

uniform and clustering-based compression baselines. These results position

STaTS as a principled, general-purpose solution for efficient, structure-aware

time series modeling.

Discussion 0