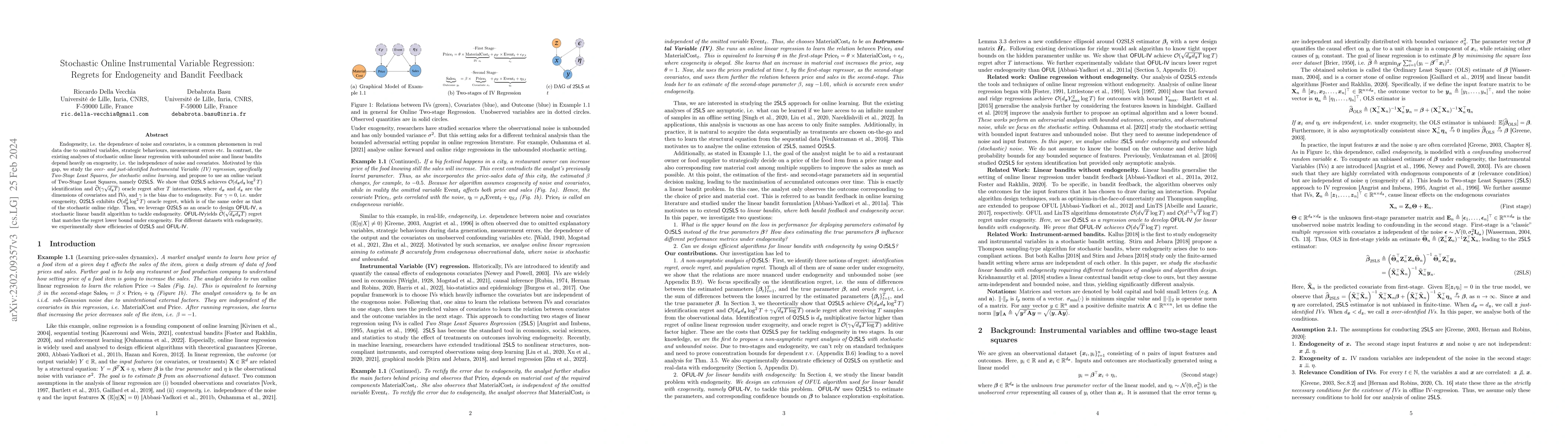

Stochastic Online Instrumental Variable Regression: Regrets for Endogeneity and Bandit Feedback

Publication

Metrics

AI Quick Summary

This paper proposes an online variant of Two-Stage Least Squares (O2SLS) for stochastic online learning to address endogeneity issues in data. It also introduces OFUL-IV, a stochastic linear bandit algorithm leveraging O2SLS to tackle endogeneity, achieving optimal regret bounds under endogeneity and demonstrating efficiency through experiments.

Paper Preview

Abstract

Endogeneity, i.e. the dependence of noise and covariates, is a common phenomenon in real data due to omitted variables, strategic behaviours, measurement errors etc. In contrast, the existing analyses of stochastic online linear regression with unbounded noise and linear bandits depend heavily on exogeneity, i.e. the independence of noise and covariates. Motivated by this gap, we study the over- and just-identified Instrumental Variable (IV) regression, specifically Two-Stage Least Squares, for stochastic online learning, and propose to use an online variant of Two-Stage Least Squares, namely O2SLS. We show that O2SLS achieves $\mathcal O(d_{x}d_{z}\log^2 T)$ identification and $\widetilde{\mathcal O}(\gamma \sqrt{d_{z} T})$ oracle regret after $T$ interactions, where $d_{x}$ and $d_{z}$ are the dimensions of covariates and IVs, and $\gamma$ is the bias due to endogeneity. For $\gamma=0$, i.e. under exogeneity, O2SLS exhibits $\mathcal O(d_{x}^2 \log^2 T)$ oracle regret, which is of the same order as that of the stochastic online ridge. Then, we leverage O2SLS as an oracle to design OFUL-IV, a stochastic linear bandit algorithm to tackle endogeneity. OFUL-IV yields $\widetilde{\mathcal O}(\sqrt{d_{x}d_{z}T})$ regret that matches the regret lower bound under exogeneity. For different datasets with endogeneity, we experimentally show efficiencies of O2SLS and OFUL-IV.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0