Publication

Metrics

AI Quick Summary

This paper proposes a method for solving stochastic optimal control problems using semidefinite programming to approximate solutions for polynomial dynamics. It leverages moment dynamics and constructs an approximate optimal control strategy by solving a semidefinite program, providing exact solutions in linear quadratic cases and increasingly accurate approximations for more complex problems.

Paper Preview

Abstract

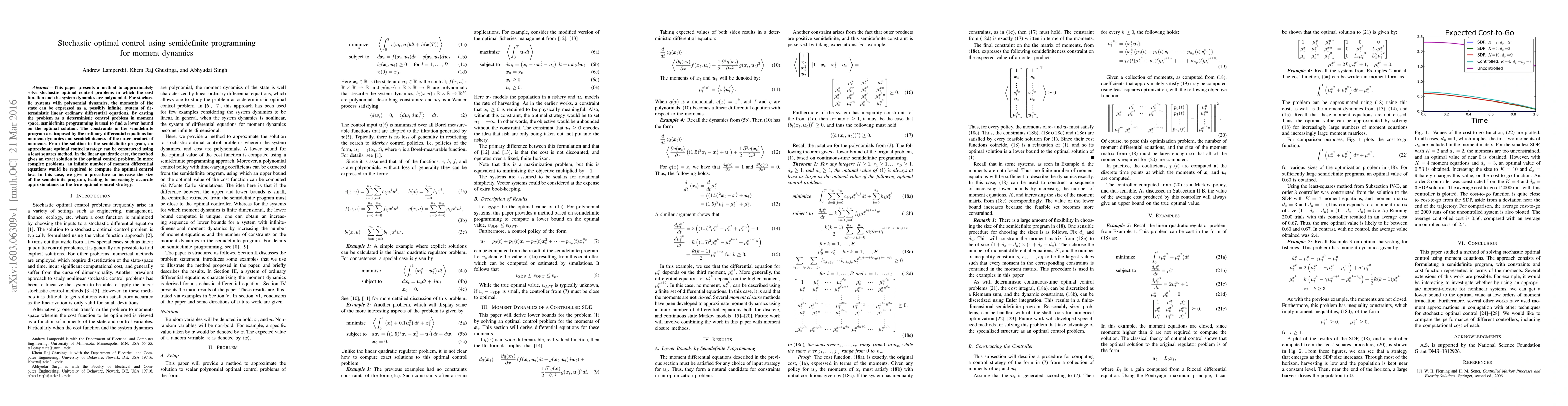

This paper presents a method to approximately solve stochastic optimal control problems in which the cost function and the system dynamics are polynomial. For stochastic systems with polynomial dynamics, the moments of the state can be expressed as a, possibly infinite, system of deterministic linear ordinary differential equations. By casting the problem as a deterministic control problem in moment space, semidefinite programming is used to find a lower bound on the optimal solution. The constraints in the semidefinite program are imposed by the ordinary differential equations for moment dynamics and semidefiniteness of the outer product of moments. From the solution to the semidefinite program, an approximate optimal control strategy can be constructed using a least squares method. In the linear quadratic case, the method gives an exact solution to the optimal control problem. In more complex problems, an infinite number of moment differential equations would be required to compute the optimal control law. In this case, we give a procedure to increase the size of the semidefinite program, leading to increasingly accurate approximations to the true optimal control strategy.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0