Stock Market Prediction Using Node Transformer Architecture Integrated with BERT Sentiment Analysis

Publication

Metrics

Paper Preview

Abstract

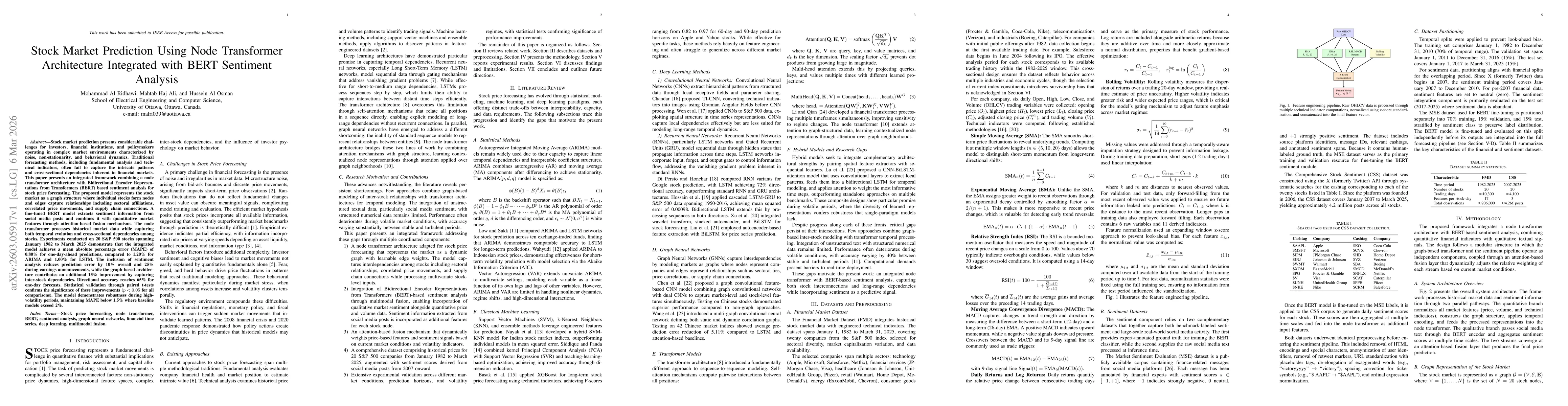

Stock market prediction presents considerable challenges for investors, financial institutions, and policymakers operating in complex market environments characterized by noise, non-stationarity, and behavioral dynamics. Traditional forecasting methods often fail to capture the intricate patterns and cross-sectional dependencies inherent in financial markets. This paper presents an integrated framework combining a node transformer architecture with BERT-based sentiment analysis for stock price forecasting. The proposed model represents the stock market as a graph structure where individual stocks form nodes and edges capture relationships including sectoral affiliations, correlated price movements, and supply chain connections. A fine-tuned BERT model extracts sentiment from social media posts and combines it with quantitative market features through attention-based fusion. The node transformer processes historical market data while capturing both temporal evolution and cross-sectional dependencies among stocks. Experiments on 20 S&P 500 stocks spanning January 1982 to March 2025 demonstrate that the integrated model achieves a mean absolute percentage error (MAPE) of 0.80% for one-day-ahead predictions, compared to 1.20% for ARIMA and 1.00% for LSTM. Sentiment analysis reduces prediction error by 10% overall and 25% during earnings announcements, while graph-based modeling contributes an additional 15% improvement by capturing inter-stock dependencies. Directional accuracy reaches 65% for one-day forecasts. Statistical validation through paired t-tests confirms these improvements (p < 0.05 for all comparisons). The model maintains MAPE below 1.5% during high-volatility periods where baseline models exceed 2%.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0