01

MethodologyHow they did it

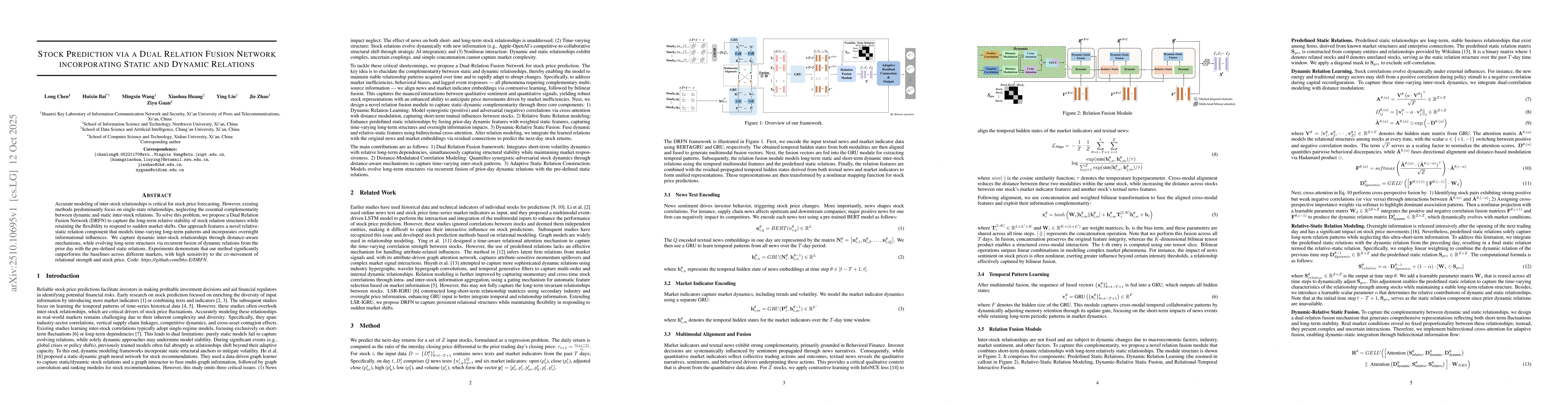

The paper proposes a Dual Relation Fusion Network (DRFN) that combines static and dynamic inter-stock relations. It uses a relation fusion module with cross-modal alignment, temporal pattern learning, and a relational-temporal interactive fusion mechanism. The model integrates predefined static relations with dynamic relations from the previous day, using attention mechanisms and bilinear transformations to capture both short-term and long-term stock relationships.

Discussion 0