Summary

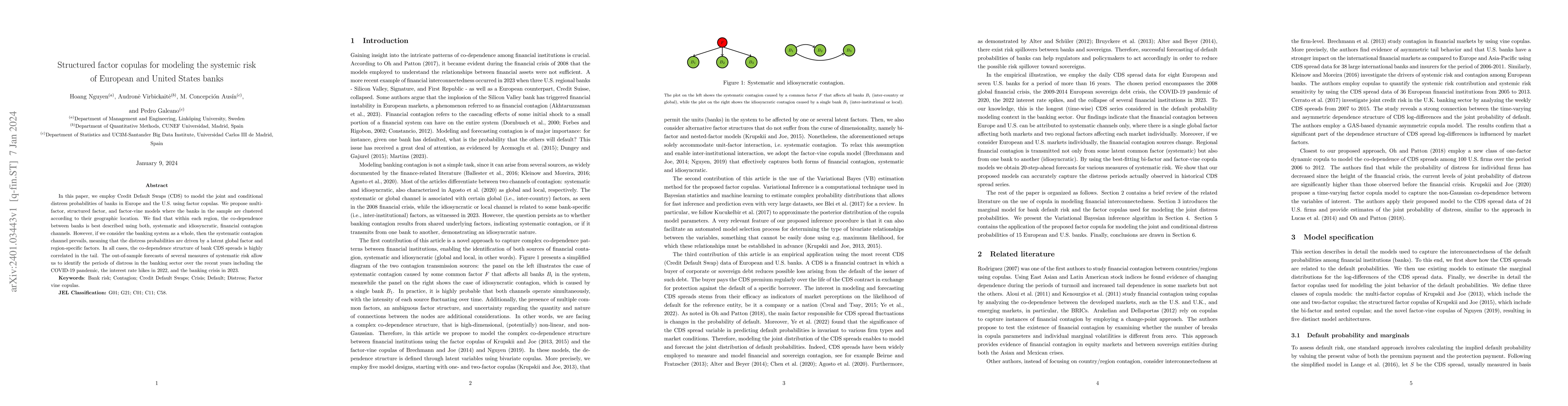

In this paper, we employ Credit Default Swaps (CDS) to model the joint and conditional distress probabilities of banks in Europe and the U.S. using factor copulas. We propose multi-factor, structured factor, and factor-vine models where the banks in the sample are clustered according to their geographic location. We find that within each region, the co-dependence between banks is best described using both, systematic and idiosyncratic, financial contagion channels. However, if we consider the banking system as a whole, then the systematic contagion channel prevails, meaning that the distress probabilities are driven by a latent global factor and region-specific factors. In all cases, the co-dependence structure of bank CDS spreads is highly correlated in the tail. The out-of-sample forecasts of several measures of systematic risk allow us to identify the periods of distress in the banking sector over the recent years including the COVID-19 pandemic, the interest rate hikes in 2022, and the banking crisis in 2023.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, and significance.

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersLarge Banks and Systemic Risk: Insights from a Mean-Field Game Model

Yuanyuan Chang, Dena Firoozi, David Benatia

| Title | Authors | Year | Actions |

|---|

Comments (0)