Supervised Dynamic Dimension Reduction with Deep Neural Network

Publication

Metrics

Paper Preview

Abstract

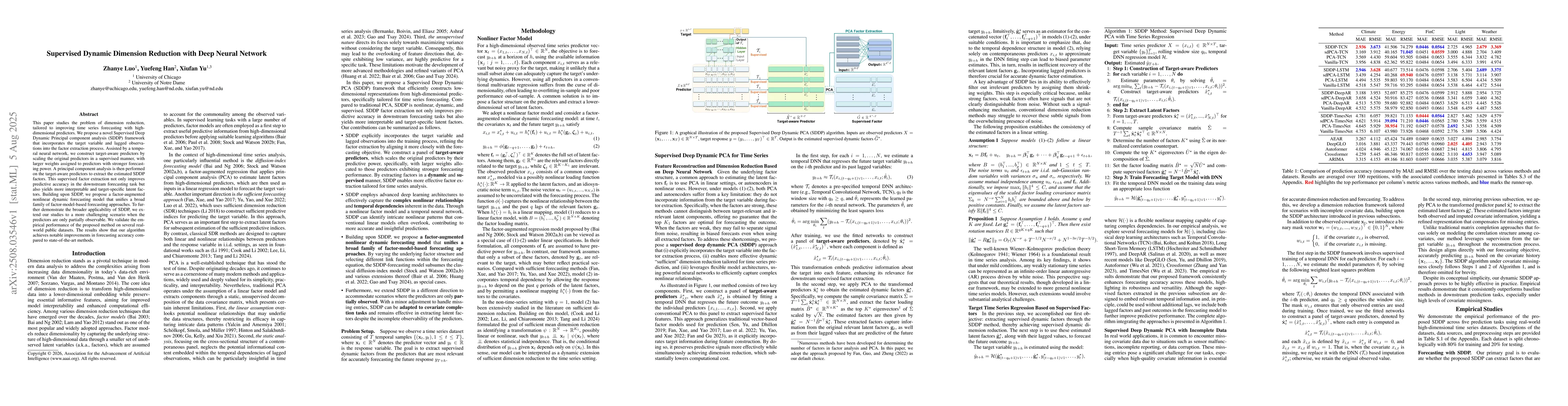

This paper studies the problem of dimension reduction, tailored to improving time series forecasting with high-dimensional predictors. We propose a novel Supervised Deep Dynamic Principal component analysis (SDDP) framework that incorporates the target variable and lagged observations into the factor extraction process. Assisted by a temporal neural network, we construct target-aware predictors by scaling the original predictors in a supervised manner, with larger weights assigned to predictors with stronger forecasting power. A principal component analysis is then performed on the target-aware predictors to extract the estimated SDDP factors. This supervised factor extraction not only improves predictive accuracy in the downstream forecasting task but also yields more interpretable and target-specific latent factors. Building upon SDDP, we propose a factor-augmented nonlinear dynamic forecasting model that unifies a broad family of factor-model-based forecasting approaches. To further demonstrate the broader applicability of SDDP, we extend our studies to a more challenging scenario when the predictors are only partially observable. We validate the empirical performance of the proposed method on several real-world public datasets. The results show that our algorithm achieves notable improvements in forecasting accuracy compared to state-of-the-art methods.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0