Temporal Latent Auto-Encoder: A Method for Probabilistic Multivariate Time Series Forecasting

Publication

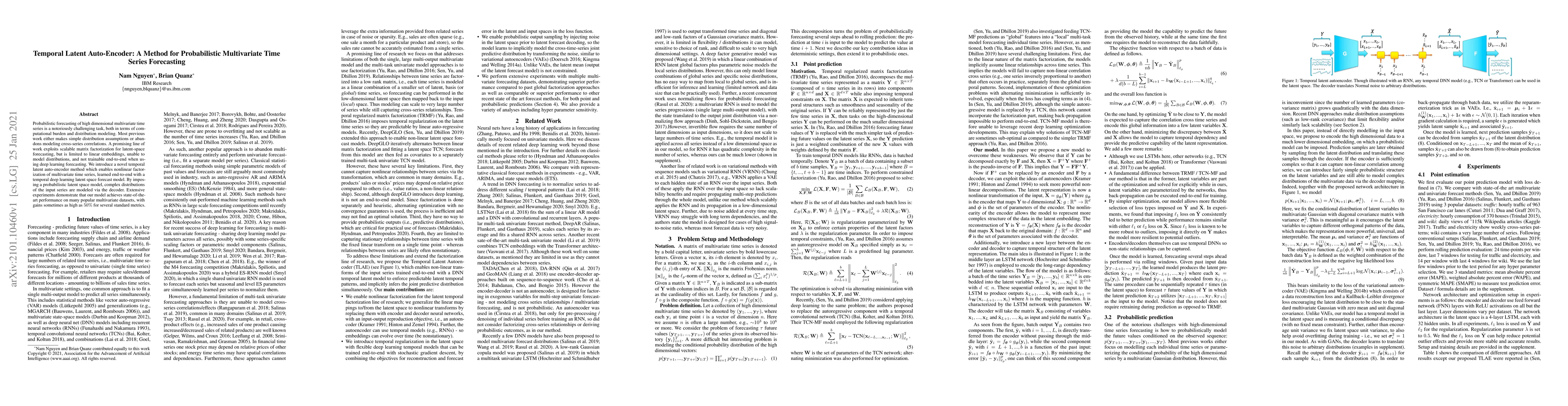

Metrics

AI Quick Summary

The paper introduces a temporal latent auto-encoder for probabilistic forecasting of high-dimensional multivariate time series, offering nonlinear factorization and end-to-end training. The method outperforms existing models on multiple datasets, achieving up to a $50\%$ improvement in standard metrics.

Paper Preview

Abstract

Probabilistic forecasting of high dimensional multivariate time series is a notoriously challenging task, both in terms of computational burden and distribution modeling. Most previous work either makes simple distribution assumptions or abandons modeling cross-series correlations. A promising line of work exploits scalable matrix factorization for latent-space forecasting, but is limited to linear embeddings, unable to model distributions, and not trainable end-to-end when using deep learning forecasting. We introduce a novel temporal latent auto-encoder method which enables nonlinear factorization of multivariate time series, learned end-to-end with a temporal deep learning latent space forecast model. By imposing a probabilistic latent space model, complex distributions of the input series are modeled via the decoder. Extensive experiments demonstrate that our model achieves state-of-the-art performance on many popular multivariate datasets, with gains sometimes as high as $50\%$ for several standard metrics.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0