Publication

Metrics

AI Quick Summary

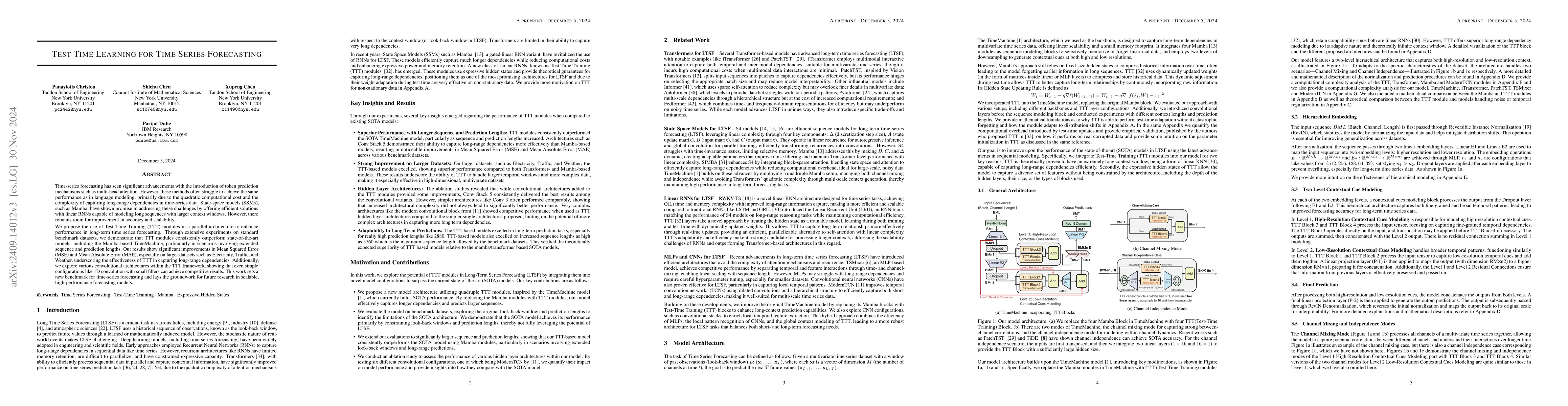

This paper proposes Test-Time Training (TTT) modules within a parallel architecture to enhance long-term time series forecasting performance. Experiments show that TTT modules outperform state-of-the-art models, particularly on larger datasets, achieving significant improvements in error metrics and demonstrating the effectiveness in capturing long-range dependencies.

Paper Preview

Abstract

Time-series forecasting has seen significant advancements with the introduction of token prediction mechanisms such as multi-head attention. However, these methods often struggle to achieve the same performance as in language modeling, primarily due to the quadratic computational cost and the complexity of capturing long-range dependencies in time-series data. State-space models (SSMs), such as Mamba, have shown promise in addressing these challenges by offering efficient solutions with linear RNNs capable of modeling long sequences with larger context windows. However, there remains room for improvement in accuracy and scalability. We propose the use of Test-Time Training (TTT) modules in a parallel architecture to enhance performance in long-term time series forecasting. Through extensive experiments on standard benchmark datasets, we demonstrate that TTT modules consistently outperform state-of-the-art models, including the Mamba-based TimeMachine, particularly in scenarios involving extended sequence and prediction lengths. Our results show significant improvements in Mean Squared Error (MSE) and Mean Absolute Error (MAE), especially on larger datasets such as Electricity, Traffic, and Weather, underscoring the effectiveness of TTT in capturing long-range dependencies. Additionally, we explore various convolutional architectures within the TTT framework, showing that even simple configurations like 1D convolution with small filters can achieve competitive results. This work sets a new benchmark for time-series forecasting and lays the groundwork for future research in scalable, high-performance forecasting models.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0