Ethereum's upcoming Glamsterdam upgrade introduces EIP-7732 enshrined

Proposer--Builder Separation (ePBS), which improves the block production

pipeline by addressing trust and scalability challenges. Yet it also creates a

new liveness risk: builders gain a short-dated ``free'' option to prevent the

execution payload they committed to from becoming canonical, without incurring

an additional penalty. Exercising this option renders an empty block for the

slot in question, thereby degrading network liveness.

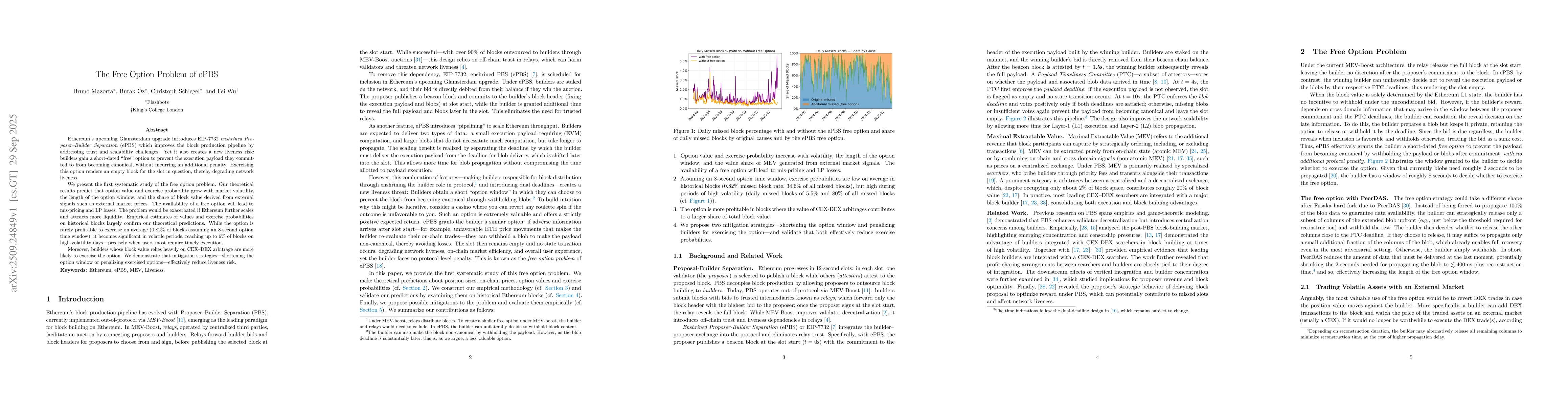

We present the first systematic study of the free option problem. Our

theoretical results predict that option value and exercise probability grow

with market volatility, the length of the option window, and the share of block

value derived from external signals such as external market prices. The

availability of a free option will lead to mispricing and LP losses. The

problem would be exacerbated if Ethereum further scales and attracts more

liquidity. Empirical estimates of values and exercise probabilities on

historical blocks largely confirm our theoretical predictions. While the option

is rarely profitable to exercise on average (0.82\% of blocks assuming an

8-second option time window), it becomes significant in volatile periods,

reaching up to 6\% of blocks on high-volatility days -- precisely when users

most require timely execution.

Moreover, builders whose block value relies heavily on CEX-DEX arbitrage are

more likely to exercise the option. We demonstrate that mitigation strategies

-- shortening the option window or penalizing exercised options -- effectively

reduce liveness risk.

Discussion 0