The study constructs a 384-month harmonized panel (1994–2025) integrating eight authoritative sources. It employs a multi-path analytical framework: (i) Demographic path with gender, skill polarization, and poverty links; (ii) Macroeconomic path examining domestic and external drivers; (iii) Time-series path using STL, ADF, KPSS, Johansen cointegration, VAR/VECM, Granger causality, impulse responses, FEVD, and machine learning forecasting. Data preprocessing includes missing-value handling, outlier treatment, normalization, log-transformations, and forward/backward filling for temporal gaps. For forecasting, Ridge Regression with lagged differenced features and external regressors is compared against SARIMA, with model selection guided by cross-validation on rolling windows. The framework also incorporates structural break consideration (2018, 2020) and uses a 12-month rolling window to compute performance metrics. The ultimate 2026 projection is conditioned on macro stability and no major Middle Eastern labor market disruptions. Data and code are made publicly available.

The Remittance Blueprint: Data-driven Intelligence for Sri Lanka

Publication

Metrics

Quick Answers

What methodology did the authors use?

The study constructs a 384-month harmonized panel (1994–2025) integrating eight authoritative sources. It employs a multi-path analytical framework: (i) Demographic path with gender, skill polarization, and poverty links; (ii) Macroeconomic path examining domestic and external drivers; (iii) Time-series path using STL, ADF, KPSS, Johansen cointegration, VAR/VECM, Granger causality, impulse responses, FEVD, and machine learning forecasting. Data preprocessing includes missing-value handling,... More in Methodology →

What are the key results?

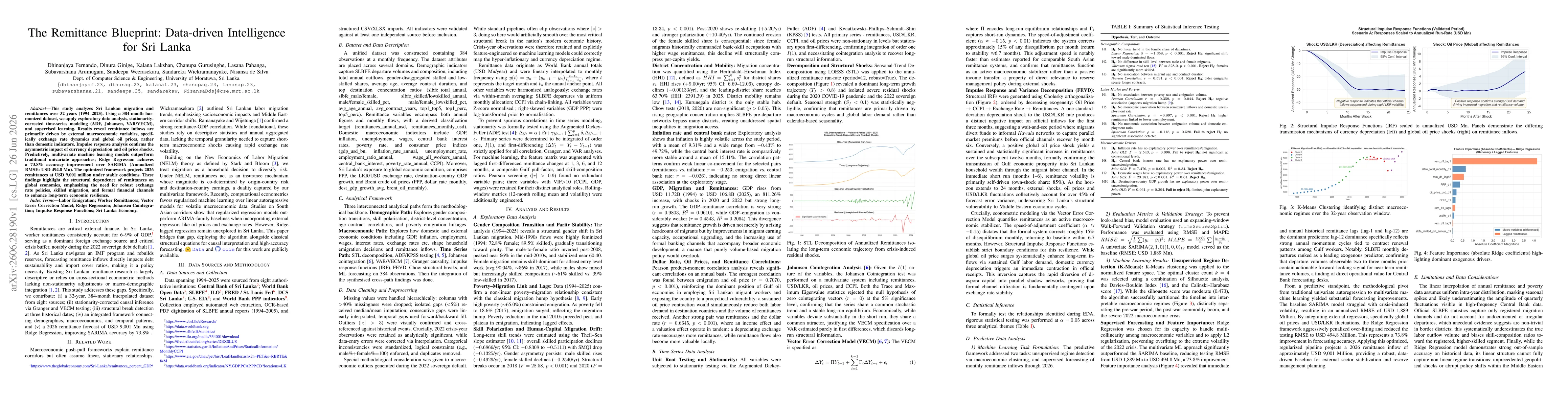

Remittances are predominantly driven by external macroeconomic variables, notably USD/LKR exchange rate dynamics and Brent crude prices, rather than domestic indicators like inflation or unemployment. — Impulse response analysis reveals asymmetric effects of currency depreciation and oil price shocks on remittance inflows, with external shocks exerting stronger short-term influence. More in Key Results →

Why is this work significant?

Demonstrates the critical role of global macrovariables in Sri Lankan remittance dynamics and provides a data-driven, cross-disciplinary framework that combines econometric causality with ML forecasting to improve predictive accuracy and policy guidance for external sector stability. More in Significance →

What are the main limitations?

Forecasting relies on macro-stability assumptions; shocks to Middle Eastern labor demand or bilateral frictions are not exhaustively modeled. — The 32-year window includes structural breaks (e.g., 2018, 2020) that may limit out-of-sample generalizability to future regimes. More in Limitations →

Paper Preview

Abstract

This study analyzes Sri Lankan migration and remittances over 32 years (1994-2025). Using a 384-month harmonized dataset, we apply exploratory data analysis, stationarity corrected time-series modeling (ADF, Johansen, VAR/VECM), and supervised learning. Results reveal remittance inflows are primarily driven by external macroeconomic variables, specifically exchange rate dynamics and global oil prices, rather than domestic indicators. Impulse response analysis confirms the asymmetric impact of currency depreciation and oil price shocks. Predictively, multivariate machine learning models outperform traditional univariate approaches; Ridge Regression achieves a 73.8% accuracy improvement over SARIMA (Annualized RMSE: USD 494.8 Mn). The optimized framework projects 2026 remittances at USD 9,001 million under stable conditions. These findings highlight the structural dependence of remittances on global economies, emphasizing the need for robust exchange rate policies, skilled migration, and formal financial channels to enhance long-term economic resilience.

Key Findings, in focus

Seven facets of this paper, analysed and brought into focus by AI.

Demonstrates the critical role of global macrovariables in Sri Lankan remittance dynamics and provides a data-driven, cross-disciplinary framework that combines econometric causality with ML forecasting to improve predictive accuracy and policy guidance for external sector stability.

- Remittances are predominantly driven by external macroeconomic variables, notably USD/LKR exchange rate dynamics and Brent crude prices, rather than domestic indicators like inflation or unemployment.

- Impulse response analysis reveals asymmetric effects of currency depreciation and oil price shocks on remittance inflows, with external shocks exerting stronger short-term influence.

- Multivariate machine learning models, particularly Ridge Regression, outperform univariate SARIMA, achieving a 73.8% accuracy improvement (annualized RMSE: USD 494.8 Mn).

- The optimized framework forecasts 2026 remittances at USD 9,001 million under stable macro conditions, highlighting structural dependence on global economies.

- Policy implications emphasize robust exchange-rate policy, expanded skill-based deployment, and formal channels to enhance resilience.

Demonstrates the critical role of global macrovariables in Sri Lankan remittance dynamics and provides a data-driven, cross-disciplinary framework that combines econometric causality with ML forecasting to improve predictive accuracy and policy guidance for external sector stability.

A unified, data-driven framework that fuses demographic, macroeconomic, and time-series analyses with regularized machine learning to forecast remittance flows and infer causal drivers in a low-to-middle-income country context.

Introduces a stationarity-corrected, multivariate approach combining VECM/cointegration with Ridge Regression forecasting in Sri Lanka, achieving substantial out-of-sample accuracy gains and delivering a 2026 remittance projection under macro-stability assumptions.

- Forecasting relies on macro-stability assumptions; shocks to Middle Eastern labor demand or bilateral frictions are not exhaustively modeled.

- The 32-year window includes structural breaks (e.g., 2018, 2020) that may limit out-of-sample generalizability to future regimes.

- All 384 monthly observations, while rich, may still constrain the complexity of deep learning architectures.

- Potential data harmonization biases across eight sources could affect comparability despite validation efforts.

- Incorporate destination-country labor-demand indicators and bilateral migration agreements to enrich causal identification.

- Integrate high-frequency and real-time data, including digital remittance flows, to enhance responsiveness to rapid shocks.

- Explore deep learning architectures and hybrid econometric-ML models to capture nonlinearities and long-term temporal structures.

- Extend regional or bilateral analyses to assess spillovers and diversification benefits for remittance resilience.

Discussion 0