The Risk Shadow of Principal Component Analysis: When 99.9999% Variance Preservation Causes Catastrophic Decision Errors

Publication

Metrics

Paper Preview

Abstract

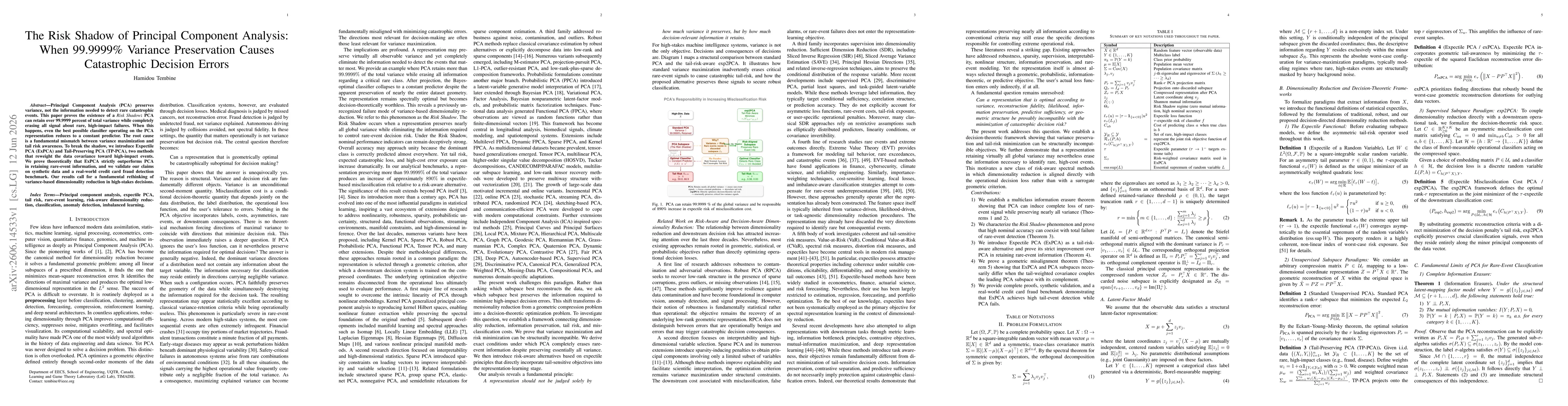

Principal Component Analysis (PCA) preserves variance, not the information needed to detect rare catastrophic events. This paper proves the existence of a {\it Risk Shadow}: PCA can retain over 99.9999 percent of total variance while completely erasing all signal about rare, high-impact failures. When this happens, even the best possible classifier operating on the PCA representation reduces to a constant predictor. The root cause is a fundamental mismatch between variance maximization and tail risk awareness. To break the shadow, we introduce Expectile PCA (ExPCA) and Tail-Preserving PCA (TP-PCA), two methods that reweight the data covariance toward high-impact events. We prove theoretically that ExPCA strictly outperforms PCA in retaining rare-event information, and we validate our claims on synthetic data and a real-world credit card fraud detection benchmark. Our results call for a fundamental rethinking of variance-based dimensionality reduction in high-stakes decisions.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0