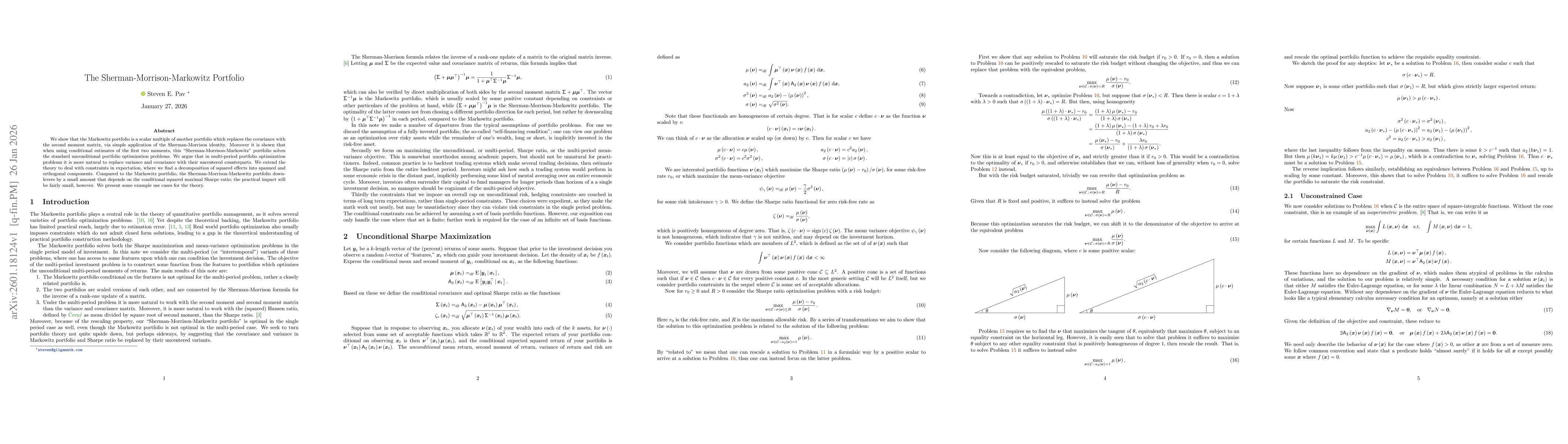

We show that the Markowitz portfolio is a scalar multiple of another portfolio which replaces the covariance with the second moment matrix, via simple application of the Sherman-Morrison identity. Moreover it is shown that when using conditional estimates of the first two moments, this "Sherman-Morrison-Markowitz" portfolio solves the standard unconditional portfolio optimization problems. We argue that in multi-period portfolio optimization problems it is more natural to replace variance and covariance with their uncentered counterparts. We extend the theory to deal with constraints in expectation, where we find a decomposition of squared effects into spanned and orthogonal components. Compared to the Markowitz portfolio, the Sherman-Morrison-Markowitz portfolio downlevers by a small amount that depends on the conditional squared maximal Sharpe ratio; the practical impact will be fairly small, however. We present some example use cases for the theory.

Discussion 0