Publication

Metrics

AI Quick Summary

The square-root impact law, previously established for stocks and futures, also applies to option markets, according to a comprehensive analysis of a large dataset of option trades. This suggests a universal underlying mechanism governing market impact across different asset classes.

Paper Preview

Abstract

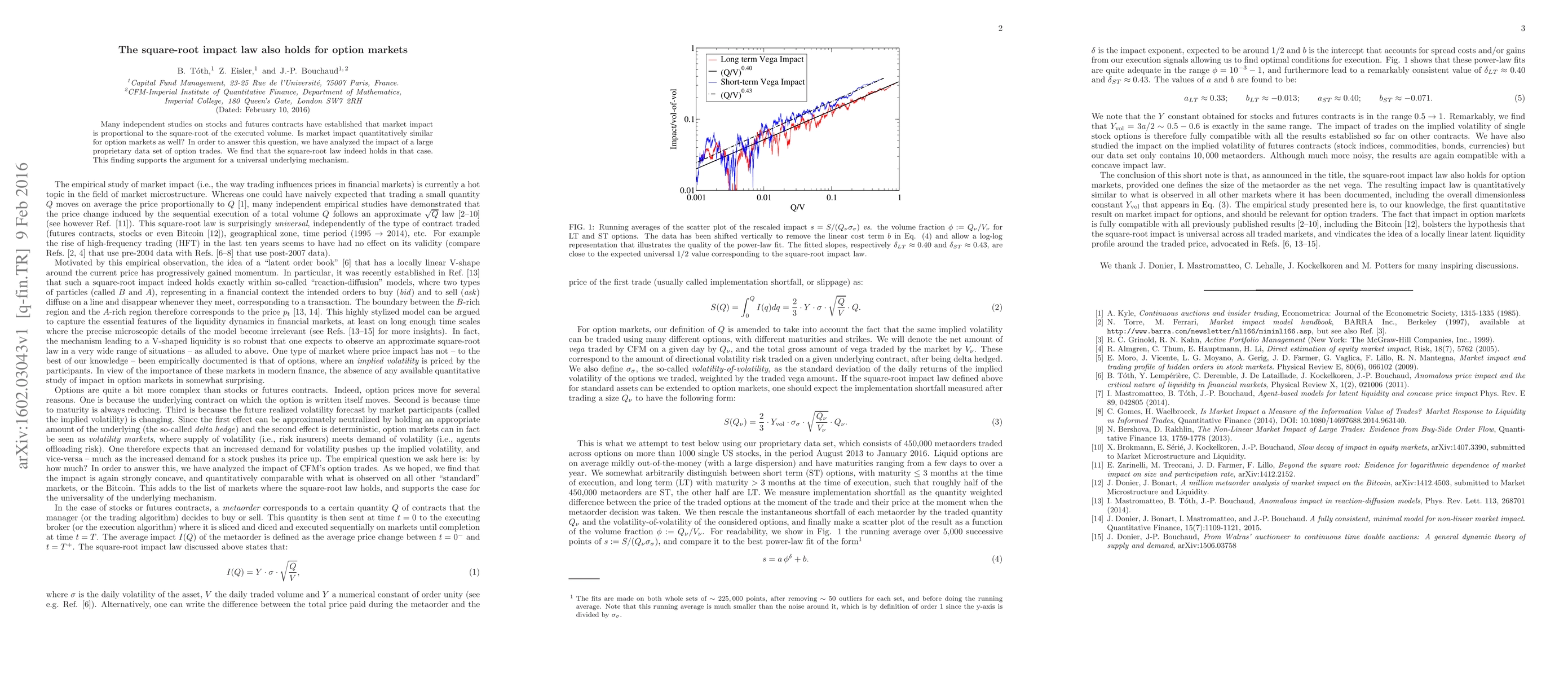

Many independent studies on stocks and futures contracts have established that market impact is proportional to the square-root of the executed volume. Is market impact quantitatively similar for option markets as well? In order to answer this question, we have analyzed the impact of a large proprietary data set of option trades. We find that the square-root law indeed holds in that case. This finding supports the argument for a universal underlying mechanism.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0