Time series forecasting with Hahn Kolmogorov-Arnold networks

Publication

Metrics

Paper Preview

Abstract

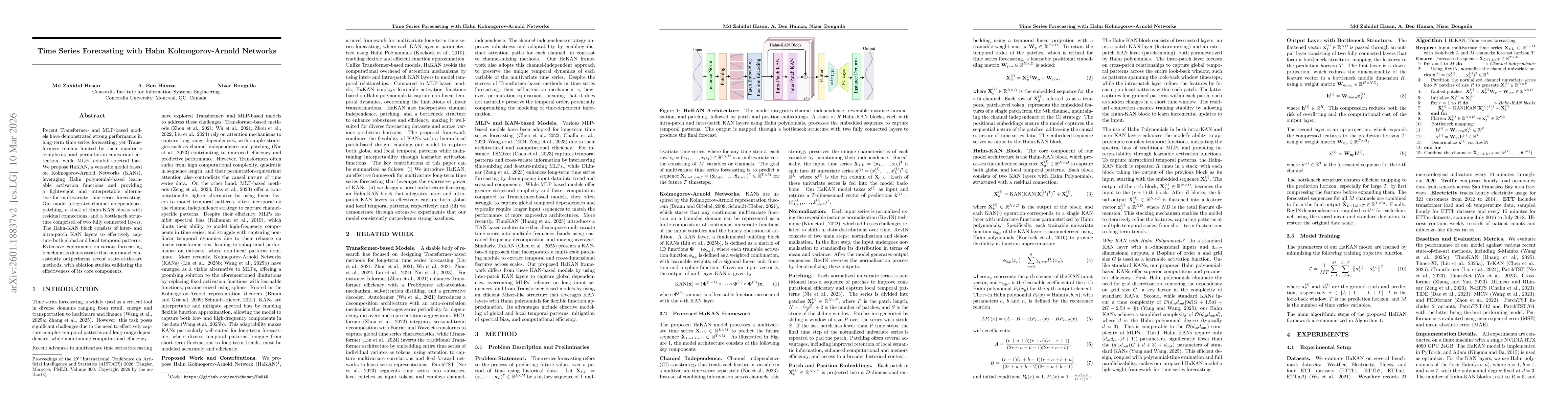

Recent Transformer- and MLP-based models have demonstrated strong performance in long-term time series forecasting, yet Transformers remain limited by their quadratic complexity and permutation-equivariant attention, while MLPs exhibit spectral bias. We propose HaKAN, a versatile model based on Kolmogorov-Arnold Networks (KANs), leveraging Hahn polynomial-based learnable activation functions and providing a lightweight and interpretable alternative for multivariate time series forecasting. Our model integrates channel independence, patching, a stack of Hahn-KAN blocks with residual connections, and a bottleneck structure comprised of two fully connected layers. The Hahn-KAN block consists of inter- and intra-patch KAN layers to effectively capture both global and local temporal patterns. Extensive experiments on various forecasting benchmarks demonstrate that our model consistently outperforms recent state-of-the-art methods, with ablation studies validating the effectiveness of its core components.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0