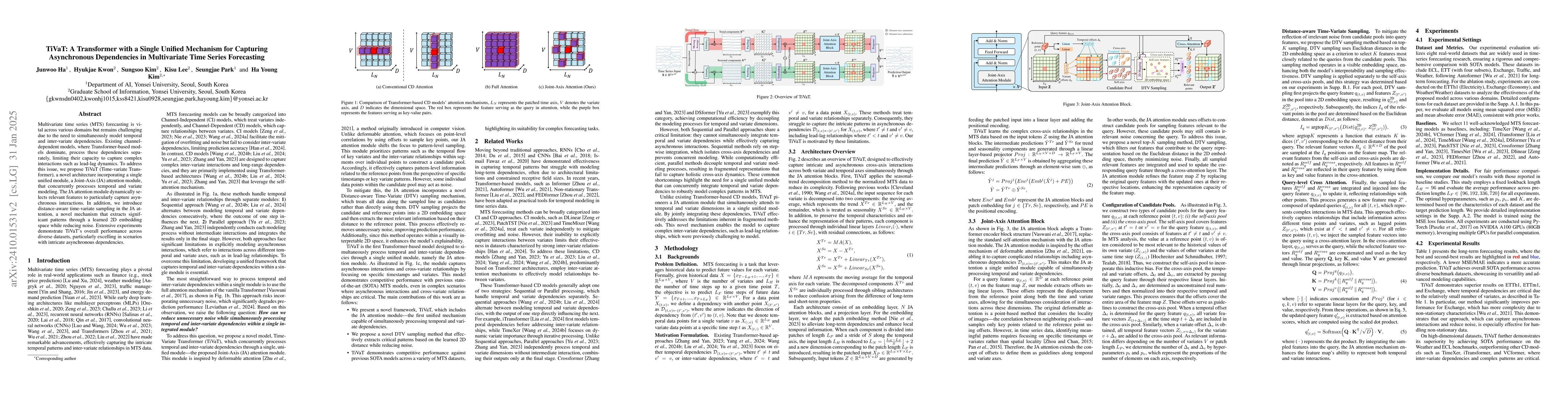

TiVaT: Joint-Axis Attention for Time Series Forecasting with Lead-Lag Dynamics

Publication

Metrics

AI Quick Summary

TiVaT, a novel architecture with a Joint-Axis attention mechanism, integrates temporal and inter-variable dependencies for multivariate time series forecasting, surpassing existing models in capturing complex lead-lag dynamics and asynchronous interactions. Its Distance-aware Time-Variable Sampling further refines interactions, establishing it as a new benchmark in the field.

Paper Preview

Abstract

Multivariate time series (MTS) forecasting plays a crucial role in various real-world applications, yet simultaneously capturing both temporal and inter-variable dependencies remains a challenge. Conventional Channel-Dependent (CD) models handle these dependencies separately, limiting their ability to model complex interactions such as lead-lag dynamics. To address these limitations, we propose TiVaT (Time-Variable Transformer), a novel architecture that integrates temporal and variate dependencies through its Joint-Axis (JA) attention mechanism. TiVaT's ability to capture intricate variate-temporal dependencies, including asynchronous interactions, is further enhanced by the incorporation of Distance-aware Time-Variable (DTV) Sampling, which reduces noise and improves accuracy through a learned 2D map that focuses on key interactions. TiVaT effectively models both temporal and variate dependencies, consistently delivering strong performance across diverse datasets. Notably, it excels in capturing complex patterns within multivariate time series, enabling it to surpass or remain competitive with state-of-the-art methods. This positions TiVaT as a new benchmark in MTS forecasting, particularly in handling datasets characterized by intricate and challenging dependencies.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0