Topological Complexity and Phase Space Stability: A Persistent Homology Approach to Cryptocurrency Risk

Publication

Metrics

Paper Preview

Abstract

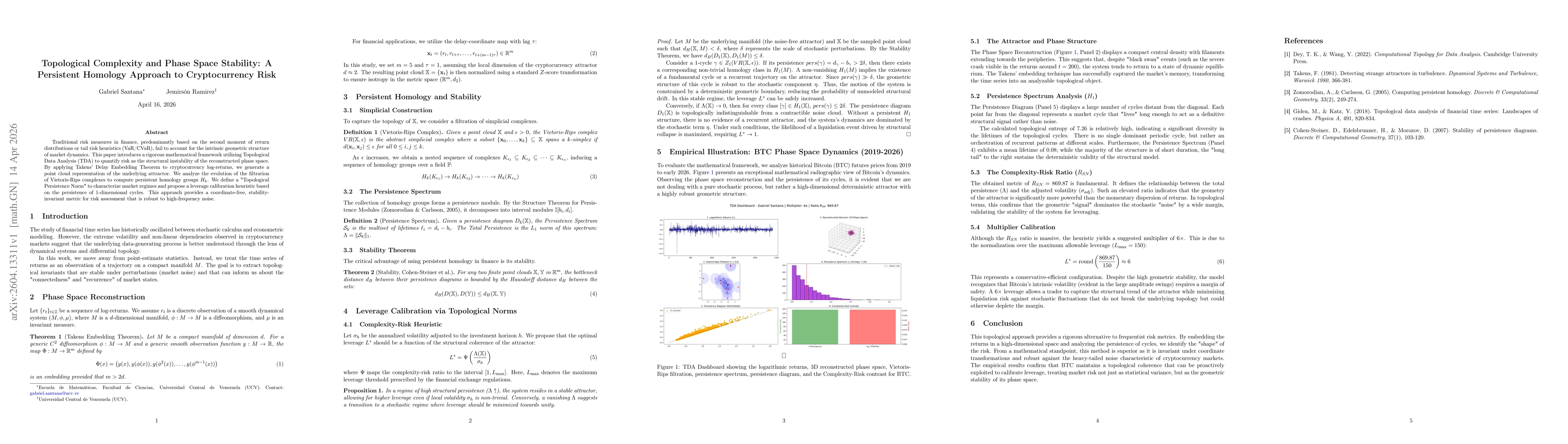

Traditional risk measures in finance, predominantly based on the second moment of return distributions or tail risk heuristics (VaR/CVaR), fail to account for the intrinsic geometric structure of market dynamics. This paper introduces a rigorous mathematical framework utilizing Topological Data Analysis (TDA) to quantify risk as the structural instability of the reconstructed phase space. By applying Takens' Delay Embedding Theorem to cryptocurrency log-returns, we generate a point cloud representation of the underlying attractor. We analyze the evolution of the filtration of Vietoris-Rips complexes to compute persistent homology groups $H_k$. We define a "Topological Persistence Norm" to characterize market regimes and propose a leverage calibration heuristic based on the persistence of 1-dimensional cycles. This approach provides a coordinate-free, stability-invariant metric for risk assessment that is robust to high-frequency noise.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0