Publication

Metrics

Paper Preview

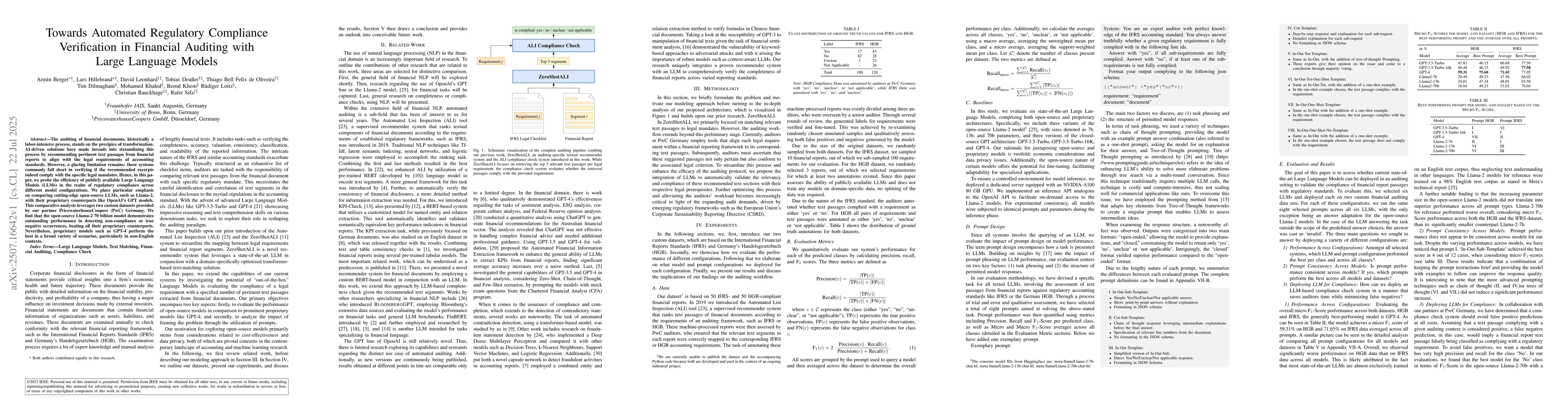

Abstract

The auditing of financial documents, historically a labor-intensive process, stands on the precipice of transformation. AI-driven solutions have made inroads into streamlining this process by recommending pertinent text passages from financial reports to align with the legal requirements of accounting standards. However, a glaring limitation remains: these systems commonly fall short in verifying if the recommended excerpts indeed comply with the specific legal mandates. Hence, in this paper, we probe the efficiency of publicly available Large Language Models (LLMs) in the realm of regulatory compliance across different model configurations. We place particular emphasis on comparing cutting-edge open-source LLMs, such as Llama-2, with their proprietary counterparts like OpenAI's GPT models. This comparative analysis leverages two custom datasets provided by our partner PricewaterhouseCoopers (PwC) Germany. We find that the open-source Llama-2 70 billion model demonstrates outstanding performance in detecting non-compliance or true negative occurrences, beating all their proprietary counterparts. Nevertheless, proprietary models such as GPT-4 perform the best in a broad variety of scenarios, particularly in non-English contexts.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0