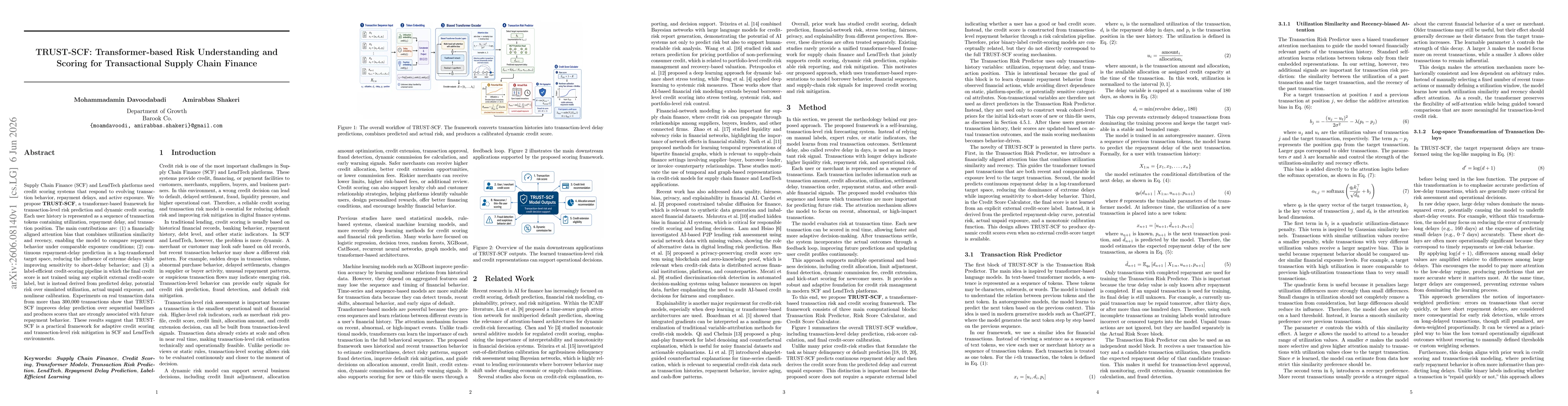

Supply Chain Finance (SCF) and LendTech platforms need credit scoring systems that respond to evolving transaction behavior, repayment delays, and active exposure. We propose TRUST-SCF, a transformer-based framework for transaction-level risk prediction and dynamic credit scoring. Each user history is represented as a sequence of transaction tokens containing utilization, repayment delay and transaction position. The main contributions are: (1) a financially aligned attention bias that combines utilization similarity and recency, enabling the model to compare repayment behavior under comparable exposure conditions; (2) continuous repayment-delay prediction in a log-transformed target space, reducing the influence of extreme delays while improving sensitivity to short-delay behavior and (3) a label-efficient credit-scoring pipeline in which the final credit score is not trained using any explicit external credit-score label, but is instead derived from predicted delay, potential risk over simulated utilization, actual unpaid exposure, and nonlinear calibration. Experiments on real transaction data from more than 300,000 transactions show that TRUST-SCF improves delay prediction over sequential baselines and produces scores that are strongly associated with future repayment behavior. These results suggest that TRUST-SCF is a practical framework for adaptive credit scoring and transaction-level risk mitigation in SCF and LendTech environments.

Discussion 0