Unconventional Policies Effects on Stock Market Volatility: A MAP Approach

Publication

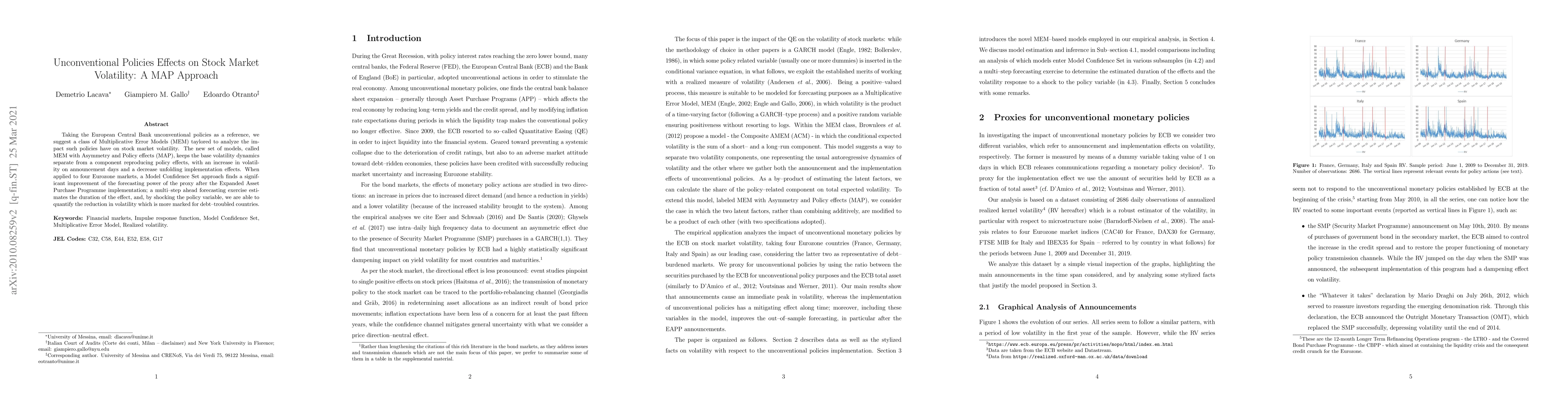

Metrics

AI Quick Summary

This paper proposes a new class of Multiplicative Error Models (MEM) with Asymmetry and Policy effects (MAP) to analyze the European Central Bank's unconventional policies' impact on stock market volatility. The MAP models show improved forecasting power post-Expanded Asset Purchase Programme, with a significant reduction in volatility, especially in debt-troubled Eurozone countries.

Paper Preview

Abstract

Taking the European Central Bank unconventional policies as a reference, we suggest a class of Multiplicative Error Models (MEM) taylored to analyze the impact such policies have on stock market volatility. The new set of models, called MEM with Asymmetry and Policy effects (MAP), keeps the base volatility dynamics separate from a component reproducing policy effects, with an increase in volatility on announcement days and a decrease unfolding implementation effects. When applied to four Eurozone markets, a Model Confidence Set approach finds a significant improvement of the forecasting power of the proxy after the Expanded Asset Purchase Programme implementation; a multi--step ahead forecasting exercise estimates the duration of the effect, and, by shocking the policy variable, we are able to quantify the reduction in volatility which is more marked for debt--troubled countries.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0