Publication

Metrics

AI Quick Summary

This paper proposes a unified principal component analysis method for spatially dependent functional data, incorporating spatial covariance estimation and functional kriging. It employs a tensor product spline estimator and demonstrates asymptotic convergence rates, validated through simulations and real data applications.

Paper Preview

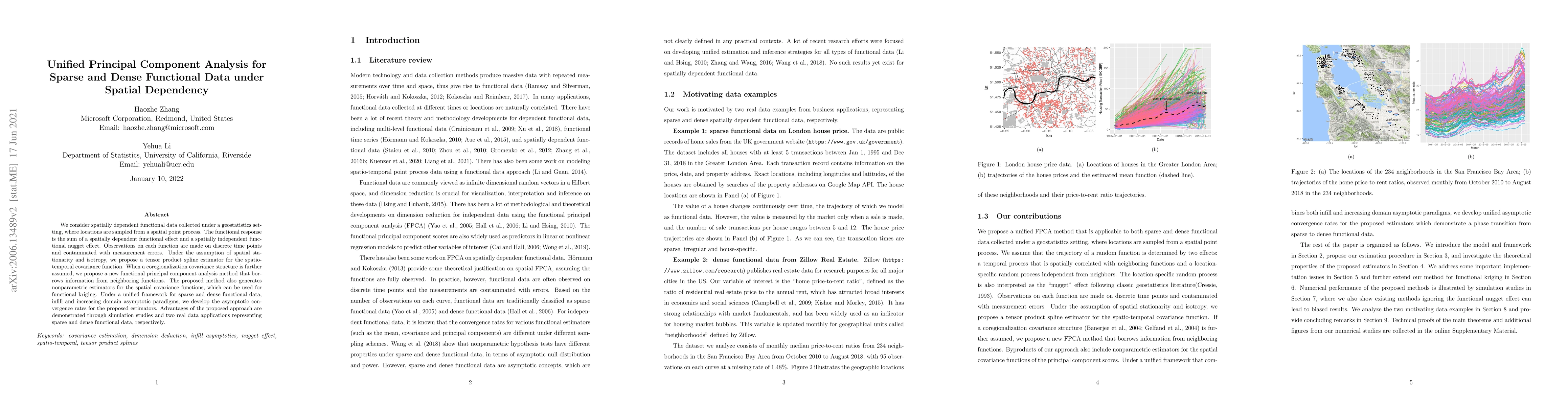

Abstract

We consider spatially dependent functional data collected under a geostatistics setting, where locations are sampled from a spatial point process. The functional response is the sum of a spatially dependent functional effect and a spatially independent functional nugget effect. Observations on each function are made on discrete time points and contaminated with measurement errors. Under the assumption of spatial stationarity and isotropy, we propose a tensor product spline estimator for the spatio-temporal covariance function. When a coregionalization covariance structure is further assumed, we propose a new functional principal component analysis method that borrows information from neighboring functions. The proposed method also generates nonparametric estimators for the spatial covariance functions, which can be used for functional kriging. Under a unified framework for sparse and dense functional data, infill and increasing domain asymptotic paradigms, we develop the asymptotic convergence rates for the proposed estimators. Advantages of the proposed approach are demonstrated through simulation studies and two real data applications representing sparse and dense functional data, respectively.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0