Using Joint Random Partition Models for Flexible Change Point Analysis in Multivariate Processes

Publication

Metrics

AI Quick Summary

A new method is proposed for detecting change points in multiple multivariate processes that share information on abrupt local changes, outperforming existing methods through improved detection of correlated change point locations.

Paper Preview

Abstract

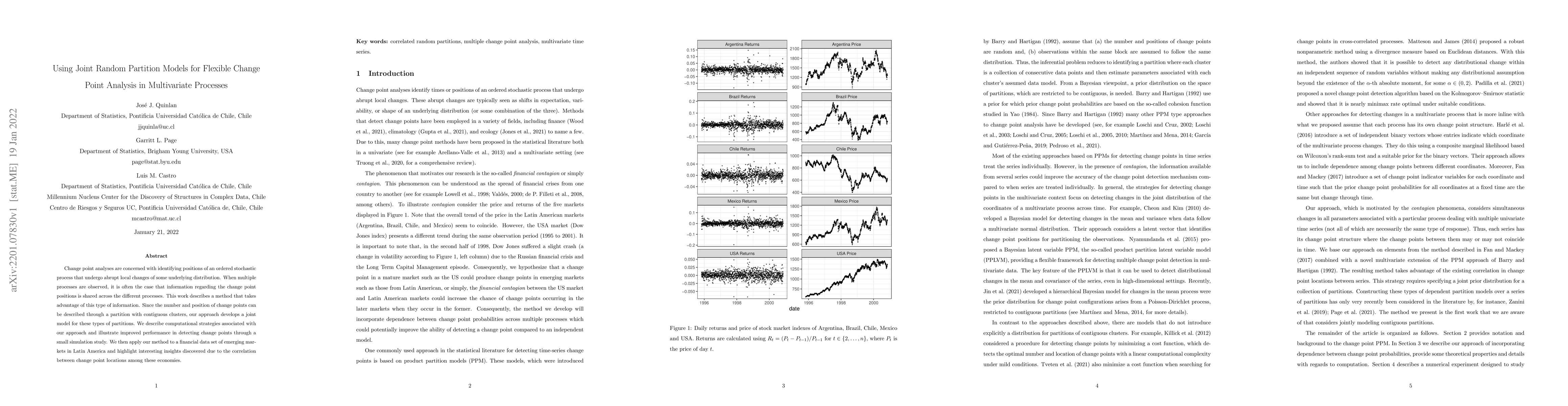

Change point analyses are concerned with identifying positions of an ordered stochastic process that undergo abrupt local changes of some underlying distribution. When multiple processes are observed, it is often the case that information regarding the change point positions is shared across the different processes. This work describes a method that takes advantage of this type of information. Since the number and position of change points can be described through a partition with contiguous clusters, our approach develops a joint model for these types of partitions. We describe computational strategies associated with our approach and illustrate improved performance in detecting change points through a small simulation study. We then apply our method to a financial data set of emerging markets in Latin America and highlight interesting insights discovered due to the correlation between change point locations among these economies.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0