Using Pre-trained LLMs for Multivariate Time Series Forecasting

Publication

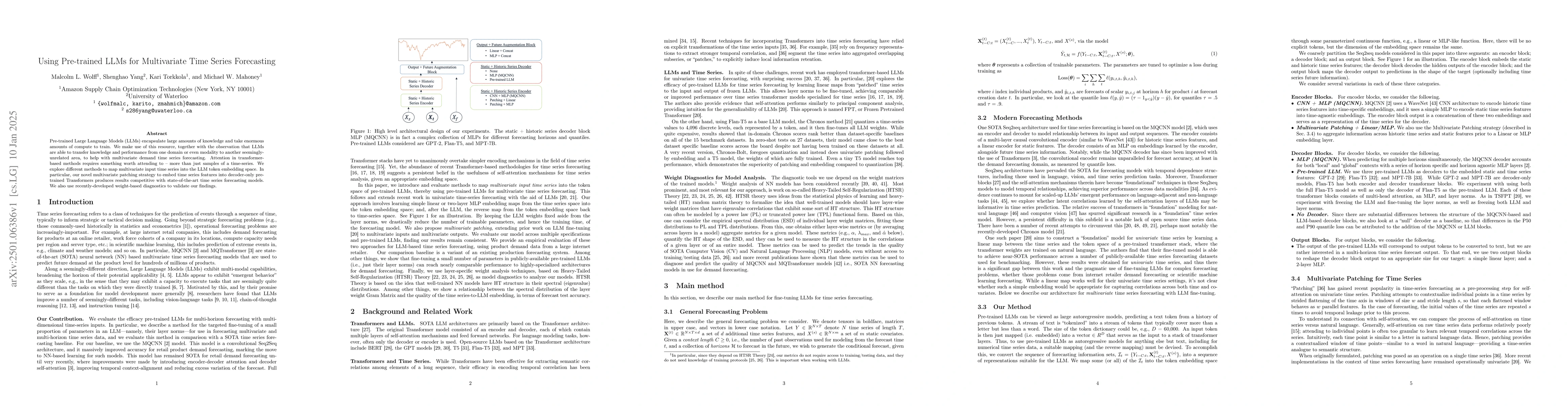

Metrics

AI Quick Summary

This paper explores leveraging pre-trained Large Language Models (LLMs) for multivariate time series forecasting by embedding time series data into the LLM token embedding space using a novel patching strategy. The approach demonstrates competitive forecasting performance against state-of-the-art models, validated with weight-based diagnostics.

Paper Preview

Abstract

Pre-trained Large Language Models (LLMs) encapsulate large amounts of knowledge and take enormous amounts of compute to train. We make use of this resource, together with the observation that LLMs are able to transfer knowledge and performance from one domain or even modality to another seemingly-unrelated area, to help with multivariate demand time series forecasting. Attention in transformer-based methods requires something worth attending to -- more than just samples of a time-series. We explore different methods to map multivariate input time series into the LLM token embedding space. In particular, our novel multivariate patching strategy to embed time series features into decoder-only pre-trained Transformers produces results competitive with state-of-the-art time series forecasting models. We also use recently-developed weight-based diagnostics to validate our findings.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0