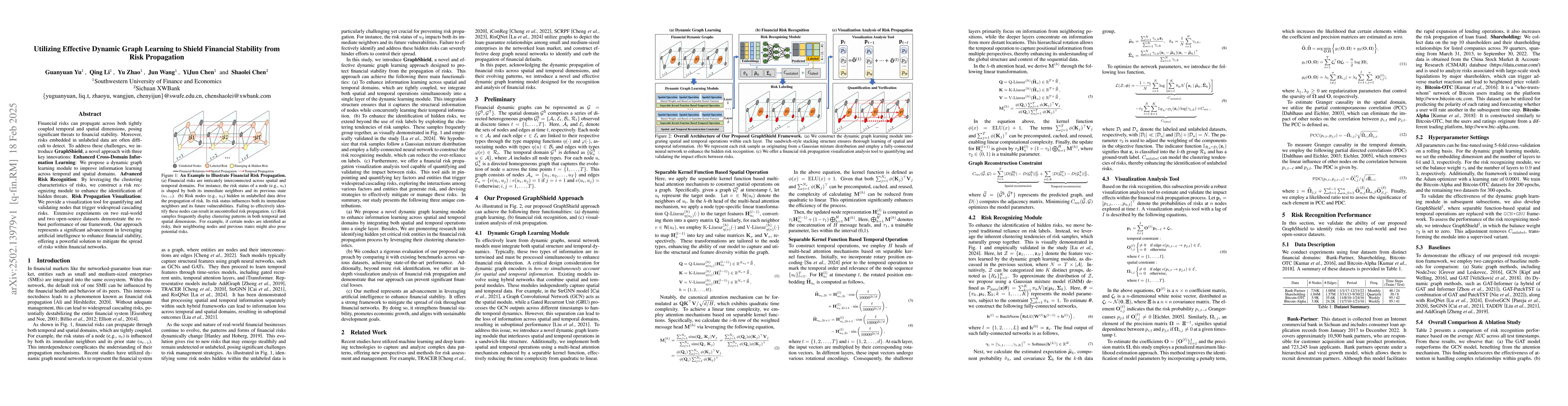

Financial risks can propagate across both tightly coupled temporal and

spatial dimensions, posing significant threats to financial stability.

Moreover, risks embedded in unlabeled data are often difficult to detect. To

address these challenges, we introduce GraphShield, a novel approach with three

key innovations: Enhanced Cross-Domain Infor mation Learning: We propose a

dynamic graph learning module to improve information learning across temporal

and spatial domains. Advanced Risk Recognition: By leveraging the clustering

characteristics of risks, we construct a risk recognizing module to enhance the

identification of hidden threats. Risk Propagation Visualization: We provide a

visualization tool for quantifying and validating nodes that trigger widespread

cascading risks. Extensive experiments on two real-world and two open-source

datasets demonstrate the robust performance of our framework. Our approach

represents a significant advancement in leveraging artificial intelligence to

enhance financial stability, offering a powerful solution to mitigate the

spread of risks within financial networks.

Discussion 0