Volatility return intervals analysis of the Japanese market

Publication

Metrics

AI Quick Summary

This paper analyzes scaling and memory effects in return intervals of price volatilities above a threshold in the Japanese stock market, finding similar statistical features to other markets. It reveals that return intervals follow a scaling function and exhibit memory effects, with consistent findings before and after the 1989 crash despite changes in return statistical properties.

Paper Preview

Abstract

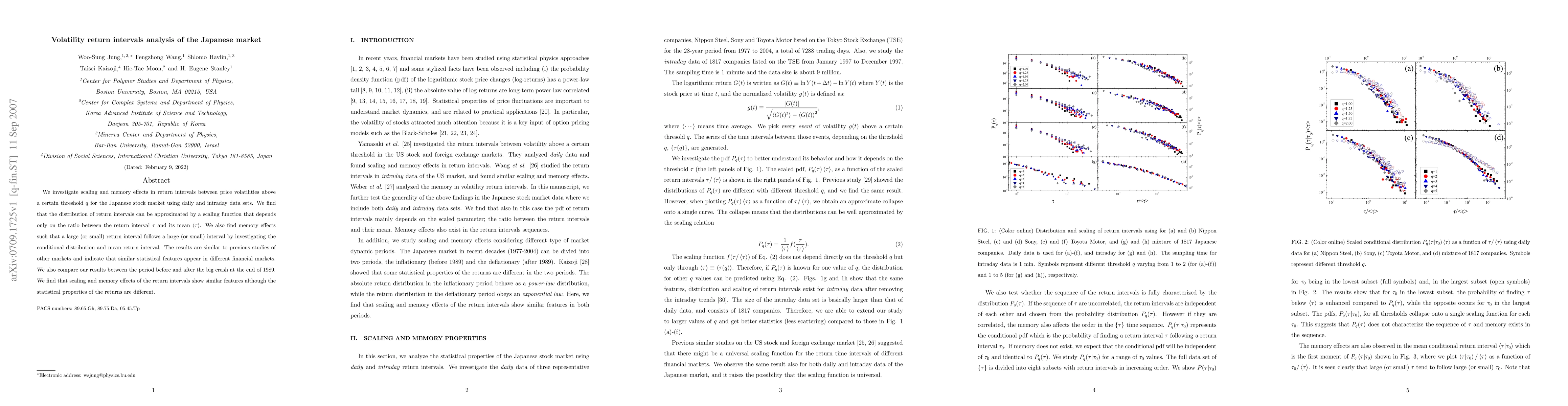

We investigate scaling and memory effects in return intervals between price volatilities above a certain threshold $q$ for the Japanese stock market using daily and intraday data sets. We find that the distribution of return intervals can be approximated by a scaling function that depends only on the ratio between the return interval $\tau$ and its mean $<\tau>$. We also find memory effects such that a large (or small) return interval follows a large (or small) interval by investigating the conditional distribution and mean return interval. The results are similar to previous studies of other markets and indicate that similar statistical features appear in different financial markets. We also compare our results between the period before and after the big crash at the end of 1989. We find that scaling and memory effects of the return intervals show similar features although the statistical properties of the returns are different.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0