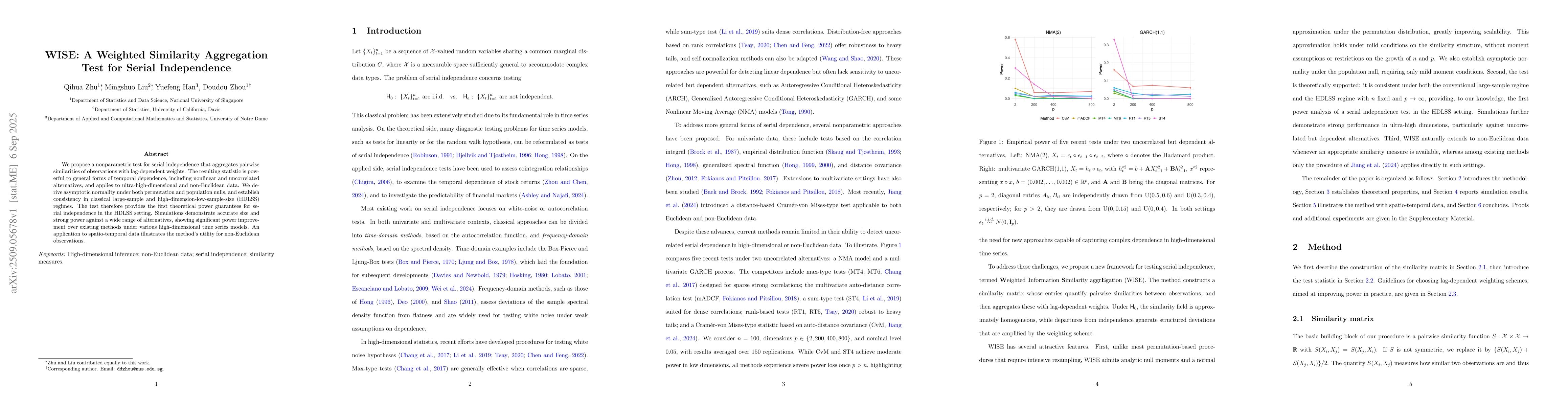

We propose a nonparametric test for serial independence that aggregates

pairwise similarities of observations with lag-dependent weights. The resulting

statistic is powerful to general forms of temporal dependence, including

nonlinear and uncorrelated alternatives, and applies to ultra-high-dimensional

and non-Euclidean data. We derive asymptotic normality under both permutation

and population nulls, and establish consistency in classical large-sample and

high-dimension-low-sample-size (HDLSS) regimes. The test therefore provides the

first theoretical power guarantees for serial independence in the HDLSS

setting. Simulations demonstrate accurate size and strong power against a wide

range of alternatives, showing significant power improvement over existing

methods under various high-dimensional time series models. An application to

spatio-temporal data illustrates the method's utility for non-Euclidean

observations.

Discussion 0